Lacker vs. Lenders - Who to believe?

Mish Moved to MishTalk.Com Click to Visit.

On April 4th, Jeffrey M. Lacker, President of the Federal Reserve Bank of Richmond presented his Economic Outlook.

Looking ahead, to assess the outlook for consumers’ spending, you begin with their income prospects. Expectations are that the overall labor market will continue to be strong: continued job growth, a moderate unemployment rate, and further real wage gains should lead to healthy advances in incomes and, thus, overall consumer spending.Phoenix Lending Survey

Before turning away from households, I’d like to touch on residential housing activity. As I’m sure you know, the housing market has had an amazing run in recent years. To cite one measure, new housing starts rose from 1.57 million units in 2000 to 2.07 million units in 2005, a remarkable 5.7 percent average annual rate of increase. And that’s just the number of housing units; on top of that, the size and quality of the average new home has been steadily increasing. Another indicator of strong demand was rising prices for existing homes. For the nation as a whole, the price of a typical single-family home rose 55 percent over the same time period.

You won’t hear me use the B-word to describe this remarkable activity. Instead, I believe fundamental factors can fully explain the expansion we’ve seen in the demand for housing, particularly rising incomes, rising population, favorable tax treatment, and very low interest rates.

Looking ahead, it seems reasonable to expect the housing market to remain strong, even as some further tapering off in sales and production takes place.

The key point I would like to emphasize is that the housing phenomenon was not a mysterious, independent boost to the economy, driven by some sort of animal spirits, but instead was a rational response by households to the economic fundamentals, especially very low real interest rates. Thus, going forward, the adjustment of the housing market to evolving fundamentals will continue to fit comfortably within the standard economic framework. My assessment is that plausible rates of moderation in housing activity will not pose a problem for overall activity this year or next. Moreover, I don’t see diminished housing price appreciation as a major problem for consumer spending, since again, the primary determinant of spending is income, and we see solid and improving prospects for real incomes for the nation as a whole.

Please compare and contrast the above rose coloured outlook with the Phoenix Lending Survey.

- Two-Thirds of Lenders Nationwide Say U.S. in Midst of Real Estate Bubble

- Half Say Burst Has Begun or Will Shortly

- 93 Percent of Lenders Predict Housing Prices Will Drop 10 - 20 Percent

Two-thirds of lenders nationwide believe a real estate bubble currently exists in the United States - and half of them believe it has already begun to burst or will burst in the next six months, according to the results of this quarter's Phoenix Management "Lending Climate in America" Survey.Hmmm. What a quandary! Who is one to believe?

A significant 93 percent of lenders surveyed expect an anticipated housing correction to result in real estate prices declining 10 to 20 percent across the country.

"In the minds of lenders, the housing bubble has moved from 'Loch Ness monster' myth status to an economic reality that could have a significant, negative impact on the lives of many Americans," said Michael E. Jacoby, Managing Director and Shareholder of Phoenix Management Services. "A year ago, 46 percent of lenders believed we were in a housing bubble. Today, that number has climbed to 66 percent - and many of them believe a correction is imminent and could lead to a drop in housing prices of up to 20 percent."

When asked when they believed the housing bubble would burst, thirty percent of lenders said it has already begun to happen. Twenty percent predicted it would occur in the next one to six months, and 27 percent thought it would happen seven to 12 months from now. Nine percent said it would occur in 2007.

Among the 92 lenders who participated in this quarter's survey, only nine percent said they did not believe a housing bubble existed.

When asked which area of the country was likely to be most affected by a housing correction, 30 percent of respondents named the Northeast, followed closely by 27 percent who predicted the West Coast. Fourteen percent named the Southeast, and five percent, each, named: the Mid-Atlantic, the Mid-West, or said all regions will be affected equally.

Half of all lenders believe a housing correction will result in real estate prices dropping up to ten percent. Forty-three percent of lenders said the decline would be as high as 20 percent.

For the first time in five years, they believe the short-term outlook for the economy is stronger than its long-term outlook.

"When we asked lenders how they expected the economy to perform over the next six months, they assigned it a high 'C' grade," Jacoby said. "But when we asked them how it would perform in the second half of 2006, they downgraded the economy to a low 'C.'

"Clearly, there are lingering concerns about whether the economy has fully rebounded in a meaningful way."

Lenders also reported lukewarm growth plans by customers. Twenty-two percent said their customers planned to make new capital investments. Sixteen percent, each, said their customers planned to: enter new markets, introduce new products or services; raise additional capital; or make an acquisition.

Only 14 percent of lenders said their customers planned to hire new employees.

About the Survey

The Phoenix Management Services "Lending Climate in America" survey is conducted quarterly to gauge shifts in lenders' attitudes toward the economy. Ninety-two lenders from commercial banks, commercial finance companies and factors across the country were surveyed this quarter. Respondents completed a written questionnaire during January and February.

Let's start here:

You won’t hear me use the B-word to describe this remarkable activity. Instead, I believe fundamental factors can fully explain the expansion we’ve seen in the demand for housing, particularly rising incomes, rising population, favorable tax treatment, and very low interest rates.

- Rising incomes? Nope - that is a lie. Real incomes have fallen since 2002. Not only that but a study put out by the Fed itself says so. Here is a report on Federal Reserve Board’s Survey of Consumer Finances.

- Rising population? Ok - but is it rising faster than it was 5 years ago in any significant way that would cause home prices to double in many locations? Nope, California is actually losing population now.

- Favorable tax treatments - Have mortgage deductions changed in the last 5 years? I think not. Capital gains exclusions did change but that is only on the primary home and that would seem to encourage cashing out rather than buying new homes if anything.

- Very low interest rates? Ding ding, we have a winner. But is that a "fundamental reason" or a the Fed blowing a bigger bubble in the aftermath of the NasCrash?

Two thirds of lenders say we are in a bubble. Most of those that do not use the word bubble still think prices are headed for a steep correction. It should not take a genius to figure that out so one has to question the mental agility of Mr. Lacker.

Why Lend?

On that note, the telepathic question lines are open for questions. Here is the main question on everyone's mind "Ok Mish, so if we are in a bubble why does everyone keep lending?" Good question. Here are the answers:

- Lenders can pass the trash. As long as they can collect an origination fee and pass the loan off to Fannie Mae or Freddie Mac or to hedge funds willing to suck up every CDO (collateralized debt obligation) they can find, lenders are quite willing to keep making real estate loans. They keep the safest of the lot and pass the trash to someone else. The Fed has unleashed a credit derivatives monster that it does not know how to stop, and it seems some like Mr. Lacker are not even aware that it exists or the effect it has had on home prices.

- If lenders think they do not have any skin in the game they will just keep lending, bubble or not. Right now, right or wrong (and I think wrong), lenders think the popping of the bubble will not affect them. When a derivative crisis unfolds (and it is only a matter of time before it does), we are going to see some lenders go under.

- One must also point out the unshaken belief right now that everyone has in the Fed. In every problem situation for twenty years, the Fed has attempted to solve the problem by throwing money at it. A pervasive attitude seems to be the Fed once again will bail everyone out in the "unlikely" event there is some sort of major blowup. It is only a matter of time before that complacency is severely tested.

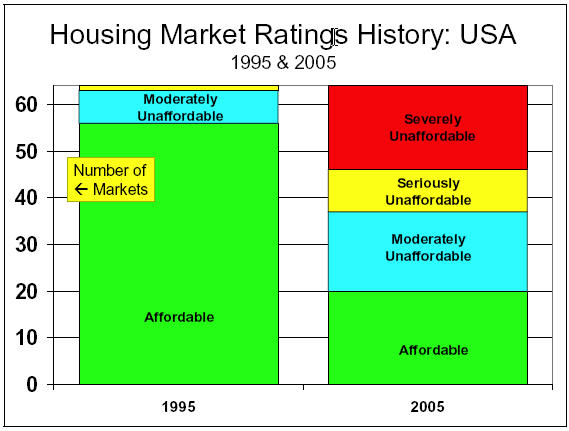

International Housing Affordability Study

I suggest everyone take a good hard look at the 2nd Annual Demographia International Housing Affordability Survey for 2006.

It is a very interesting study and as best as I can tell unbiased. Following is one of my favorite charts from the article.

Many analysts and much of the business press have followed the unprecedented housing cost price escalation with seeming glee, while ignoring the reality that household incomes have not been inflating at a corresponding rate. This superficial approach is both naïve and irresponsible. Any number of products might be imagined that might be converted into objects of financial speculation, at the same time as rendering a nation less prosperous. For example, massive and unprecedented price escalation, from speculation in food products or medical markets might serve the short-term interest of investors, while imposing broad detrimental effects. There is a public interest in maintaining house prices within the economic means of most households.The study goes on to propose that land use restrictions are the big reason behind this rise, with charts to prove it too, but in general I have to question that theory.

Oddly, the most affordable markets have sometimes been characterized as poor performers. There are many losers when home prices become decoupled from the underpinning income realities. Middle income and lower income households find it impossible to afford the higher prices and may be relegated to renting for many additional years, if not a lifetime. The equity that they would have built up instead goes to the pockets of landlords. Others fortunate enough to afford the higher prices must settle for more modest houses, which are likely of lower quality.

Some analysts have noted that, by mortgage qualification standards, housing affordability is no worse than in the early 1980s. However today’s unaffordability is different. The unaffordability of the early 1980s was due to high interest rates. As interest rates declined, households refinanced the debt on their homes at lower rates, improving affordability. This made the 1980s unaffordablity inherently temporary, even for those who purchased at the most unfavorable time.

Unaffordability, however, is not temporary for households who purchase homes at the excessively high prices typical of the highly regulated markets. By reducing the share of households that can afford to buy homes, high Median Multiples inevitably lead to greater income disparity. Thus, to think of rising house prices as a good thing while ignoring the incomes that support them is to miss the point completely. Australian Reserve Bank Governor Ian MacFarlane emphasized this point in parliamentary testimony with reference to the unaffordable housing prices in Sydney. The reality, of course, is that the more affordable markets are the better performers by virtue of the higher standard of living that they facilitate for more households. However, the reality is that declining housing affordability has reached crisis proportions in many markets.

Have land use restrictions dramatically changed in Boston, San Diego, Las Vegas, Florida, Phoenix, etc, in the last 5 years (places where prices have doubled in that time frame)?

If not, then why would land restrictions cause a sudden explosion now as opposed to a gradual escalation over time? Would the problem go away if all restrictions were removed in LA? I think not.

Perhaps a better answer is that manias simply got more carried away in some parts of the country than others for a multitude of reasons. The study did not mention proposition 13 or low property tax rates in Florida (at least I did not see it if they did). Las Vegas and Phoenix did participate in a big way in the bubble but as best as I know land was plentiful around Las Vegas and plentiful around Phoenix as well.

If land use is such an overriding factor then one would have to say that California will not crash. Does anyone buy that theory? I don't. Did lack of land stop prices from crashing in Japan?

The progression of events seem to have been something like the following

- 1% interest rates kicked off the mania.

- People looking ahead to retirement started buying homes in warm places.

- The bigger the price increases, the bigger the mania and the more people wanted in.

- Those sitting on the sidelines and burnt by the Nasdaq crash started chasing the expanding housing bubble.

- Cash out refis accelerated whatever trend there was in place.

- Credit lending standards fell through the floor.

- Buy now before it's too late mentality kicked in. The bigger the bubble the bigger the panic buying until the supply of stupid buyers exhausted itself.

- Rust belt places losing jobs did not participate whether or not land use restrictions were in place.

Let's now return to the original question:

Lacker vs. Lenders - Who is one to believe?

Is it close?

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/