Jobs and wages during the recovery

Mish Moved to MishTalk.Com Click to Visit.

This post takes a look at the effectiveness of the Bush administration tax cuts, jobs, wages, housing, and the "Bernanke Handoff".

The charts below are thanks to the Economic Policy Institute.

Here goes:

Failure of the Bush tax cuts

Changes in tax law since 2001 reduced federal government revenue by $870 billion through September 2005. Supporters of these tax cuts have touted them as great contributors to growth in jobs and pay. But, in reality, private-sector job growth since 2001 has been disappointing, and a closer look at the new jobs created shows that federal spending—not tax cuts—are responsible for the jobs created in the past five years.

If tax cuts have created jobs at all since 2001, it will have happened in the private sector. Assuming that job growth in 2006 matches the Bush Administration's projections, the economy will have added about 2.0 million jobs to the private sector from FY2001 through FY2006. But how many of these two million jobs actually can be attributed to tax cuts and how many to increased government spending—particularly increased defense spending—in this period?

Based on Defense Department estimates of the number of private-sector jobs created by its own spending, we project that additional defense spending will account for a 1.495 million gain in private sector jobs between FY2001 and FY2006. Furthermore, increases in non-defense discretionary spending since 2001 will have added yet another 1.325 million jobs in the private sector, for a total of 2.82 million jobs created by increased government spending. Increased mandatory government spending—which is not even included in these estimates or the accompanying chart—would account for even more job creation. The mere fact that the projected job growth resulting from increased defense and other government spending exceeds the actual number of jobs projected to be added to the economy through 2006 clearly indicates that the tax cuts hardly seem plausible as the engine of the modest job growth in the economy since 2001.

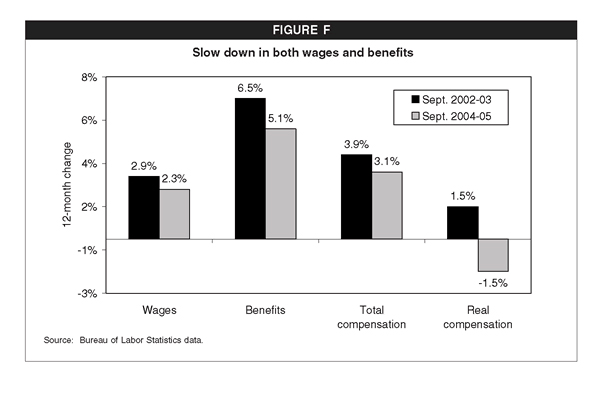

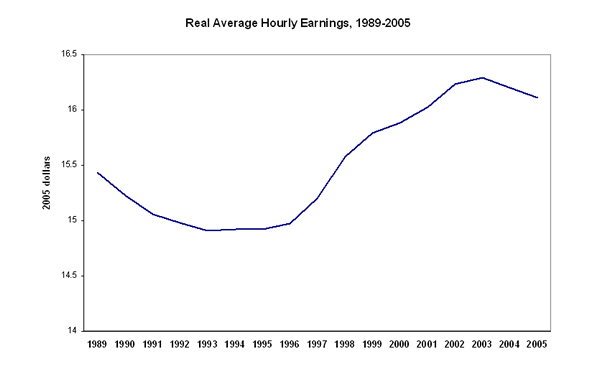

Why people are so dissatisfied with today's economy

Real wages were down for the second full year in 2005

Adjusted for inflation, hourly and weekly earnings fell for most workers in 2005

Real earnings growth flat to negative in 2003

Very negative since then

Thanks again to the Economic Policy Institute.

The question is: where to from here?

Treasury secretary Snow and Bush both point to a continued recovery, but the above data suggest that is only possible if government spending picks up. Consumers are showing signs of severe stress with each and every hike. Some think that capex spending will save the day but as discussed in Thoughts on the Handover Fallacy, that seems highly unlikely.

With negative savings and cash-out refis withering on the vine, only the stock market, rising wages, or a renewed housing bubble can save consumer spending. The latter two choices seem unlikely. Global wage arbitrage is still putting severe pressure on wages and benefits.

Housing itself is like a supertanker. Supertankers are very slow to change direction, and once they do, much harder still to immediately turn back around. The housing supertanker has now turned. The top is in.

That leaves the stock market. Unfortunately for stock market hopefuls there are a multitude of problems:

- Studies suggest consumers are more likely to spend housing gains than stock market gains.

- A flat to negative yield curve is not conducive to corporate earnings growth.

- This recovery is actually quite long by historical standards.

- The second year election cycle suggests a slowdown.

- Global wage arbitrage and outsourcing still seem to be going strong.

- A cutback in Iraq war spending is now underway.

- Energy and medical expenses continue to cut into consumer discretionary consumer spending.

- 1/3 of the houses sold in 2004 were second home or for investment. That is not sustainable.

- Housing fire sales such as housing fire sales suggest declining consumer speculation. Those are on top of Poof - 25% Underwater Overnight fire sales.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/