A Tsunami Wave of Foreclosures

Mish Moved to MishTalk.Com Click to Visit.

Mark Ijlal on his Profitable Investment In Bank Owned Foreclosures website writes:

"I remember 5 years ago when Darrick used to walk in, waving the foreclosure list in his hands and saying look we got a nice suburban house here for around $150,000, lets check it out. And now you can pretty much find couple of million dollar foreclosures every month, without looking."

"The thing that amazes me is how fast things have gone from 100 foreclosures per month per county to all of sudden couple of hundred foreclosures coming in month after month in almost every county."

That quote sums it all up nicely: foreclosures, even at the high end are soaring. Can everyone flip million dollar foreclosures for a profit? I guess so, but at this stage in the game, I think I'll take a pass. The real question is this: How come foreclosures are soaring if the economy is 3 years into a recovery and leading economic indicators are near all time highs? No doubt that is another economic conundrum puzzling Greenspan these days.

Well just how bad is it? That's a fair question and enquiring Mish Blog readers deserve answers. Let's take a look:

Houston foreclosures rise in record year

A record year for construction of new homes in Houston was offset by a negative side effect as the number of residential foreclosures increased sharply in 2004. A total of 19,866 homes were posted for foreclosure in Harris County, a significant jump from the 17,230 posted in 2003, according to the Foreclosure Listing Service.

Amanda LeCureux of the listing service says the number of postings in 2004 was the highest total the company had seen since mid-1989. While foreclosures were climbing, new single-family home starts reached 42,000, breaking the 40,000 barrier for the first time in city history.

Housing boom brings surge of foreclosures to Nashville area

The number of home foreclosures for Davidson and nine surrounding counties rose 52% to 3,004 last year, up from the 1,976 recorded in 2003. Credit counselors and others who work with people in financial distress said the surge in foreclosures adds a dark cloud to the otherwise sunny picture of a housing boom enjoyed locally and nationally since 2000. They say the numbers also point to the dangerous game many middle- and lower-income Americans are playing: living paycheck to paycheck while saddled with debt.

"A lot of Americans are living paycheck to paycheck," observed Howard Dvorkin, founder of the nonprofit Consolidated Credit Counseling Services Inc. in Fort Lauderdale, Fla. "We're spending every dollar we have. And then something happens in their life to cause them to fall off that tightrope."

Metro Denver area foreclosures up 34 in 2005%

Soaring foreclosure filings in Arapahoe County for the first three months of this year helped drive metro Denver's foreclosure rate 34 percent higher than the same period of last year and 30 percent higher than the fourth quarter of 2004.

The seven-county region's ballooning rates stem from bad borrowing and lending decisions, lagging income growth and flat home prices, experts say.

It's hard to continue blaming foreclosures only on the economy. Colorado added 27,900 jobs last year, and the state's unemployment rate dropped in January to 4.9 percent, the lowest level since September 2001.

Read that last sentence again. Then read it again.

How do massive increases in foreclosures jive with all this "ballyhooed job growth" and "things are getting better" BS coming from the FED and the Whitehouse? That my friends is the REAL conundrum that the FED should be worried about instead of pondering why long terms rates have not risen. Perhaps long term rates have not risen much is because there is far far more stress in the system than the FED is aware of!

What is anyone doing about it? Good question! Enquiring Mish readers might want to consider this:

Pa. Bank Chief Seeks to Stem Foreclosures

Pennsylvania's banking secretary said Tuesday he will press for new laws and regulations to stem a surge of home foreclosures that he said were due in part to unscrupulous lending practices.

Bill Schenck said the Banking Department believes it can reduce the state's mortgage foreclosure rate, one of the nation's worst, by focusing on sub-prime lending loans issued at higher rates and larger fees to customers with relatively poor credit. Pennsylvania is one of a number of states that have been hard-hit by foreclosures in recent years as home ownership opportunities have expanded, including for people with poor credit. Sub-prime loans are most prevalent in low-income and minority neighborhoods.

What is President Bush doing?

Zero-percent down home loans spark debate

"To boost homeownership among minorities and immigrants, the Bush administration has asked Congress to allow the FHA to insure mortgages with no down payment for first-time home buyers. Zero-down loans could carry a lot of risk. FHA Commissioner John Weicher told the House Financial Services Committee that, over the life of the loans, 17 percent of zero-down borrowers - about one in six - would be foreclosed on or be forced to sell their homes at a loss. In contrast, the estimated cumulative default rate for all FHA loans originated this fiscal year is 6.96 percent. "

Now that's interesting isn't it? The FHA commissioner estimates that 17% of zero down borrowers will fail. Who will pay the price? Taxpayers of course? Who else? Marginal people attempting to buy a home! Yes, that's correct: the very program designed to "help the poor" in this nonsensical "ownership society" is one of the factors that has driven housing to unaffordable levels. Of course the banks and FNM are all in favor of such programs. Who wouldn't be? After all, what lender would refuse to lend with the government backing the loan? Doesn't it seem that Pennsylvania's banking secretary and the FHA commissioner have radically different views than Bush as to what the real problem is?

Is there more?

That is of course another fair question and another question that enquiring Mish readers deserve an answer to. Yes indeed there is more.

Consider bankruptcy reform.

All of the lenders are in favor of it. Why not? It happens to be the most one sided bill in history. Short of reviving debtor prisons this bill is about as regressive as it gets. Lending institutions want protection against default, they want no restrictions on charging 30% interest rates, they want no restrictions on fees, penalties or anything else, and they want the proverbial "free lunch". The "free lunch" bill seems all greased up ad ready to go. It was the worst legislation that money could buy. In the meantime, the FHA and Pennsylvania's banking secretary warn about defaults and predatory lending. Go figure.

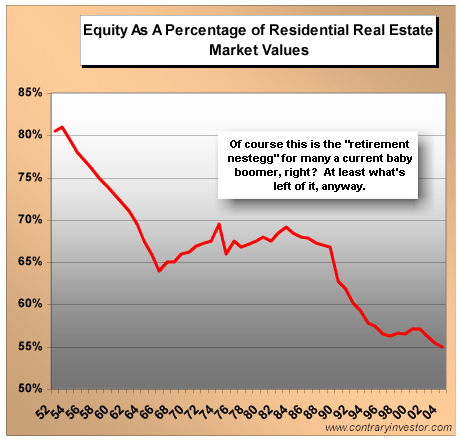

Unfortunately, the REAL Tsunami Wave of Foreclosures has not even started. Rising property values in California, Florida and other places have kept (for now) the consumer buoyant. Round after round of cash out refis has supported consumption. The REAL Tsunami starts when home equity in California and Florida goes negative. Let's consider a chart before wrapping things up:

Thanks to Contrary Investor

In spite of massively rising home prices, the percentage of home equity is at historic lows. Please bear in mind those are averages! There are many people with paid off houses. There are also tons of people leveraged in multiple houses at 100% financing and praying that home prices keep rising.

As discussed earlier there are already many areas of the country that are experiencing record forecloseures in spite of those rising home prices. What is happening is clear: The costs of home ownership (mortgage, property taxes, etc) as well as rising expenses such as food gasoline, and medical expenses are rising far faster than wages.

Over the long haul, real estate prices simply can not rise above local wages! I do not care about arguments such as: the scarcity of land, interest rates are low, boomers need a place to live, etc etc etc. over the long haul, simple logic dictates that prices simply can NOT stay above wages for a prolonged period of time. There will be hell to pay for this bubble when it pops. For now, in areas where home prices are still going up, equity extraction is still supporting consumption.

Given the 100%+ financing, speculators buying property sight unseen, multiple flips per day on a single house, and all of the other lunacies we have seen lately tells me to expect the "real upsurge" in foreclosures will start when the biggest of the big bubble areas (California & Florida) pop. That might be any time now, or it might be next year. It is very hard to tell with manias and we are clearly in one right now. Many people will be underwater when the tide turns.

In the meantime the FED seems bound and determined to "bring it on" with its new found inflation fighting warnings. Each hike (and once again I admit this has taken far more than I thought) brings us closer and closer to the edge of a massive "Tsunami Wave of Foreclosures". At this point there is nothing that anyone, including the FED, can do to prevent it.

Yes readers, it is 2000 all over again, this time in housing. Blame the FED when it happens, not for popping the bubble after the fact, but for blowing bubble after bubble after bubble in the first place.

Mish