Market Cheers 1.6% Growth; Treasuries Hammered; What's Next?

Mish Moved to MishTalk.Com Click to Visit.

Today the DOW has crossed the 10K line for the umpteenth time (at least 3 times in the past 3 days alone depending on how you count), smack on the heels of "fantastic news" that second quarter GDP was 1.6%.

For a change, economists were a bit too pessimistic but to get to that point, their estimates had to be ratcheted down twice from 2.5% to 1.4%. Now the market, temporarily at least, thinks 1.6% is good.

It isn't. More importantly, GDP expectations looking forward for 3rd quarter are in the neighborhood of 2.5%, a number that is from Fantasyland. I expect a negative print.

GDP News Release

Inquiring minds are digging into the BEA's report National Income and Product Accounts

Gross Domestic Product, 2nd quarter 2010 (second estimate) for additional details.

Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- increased at an annual rate of 1.6 percent in the second quarter of 2010, (that is, from the first quarter to the second quarter), according to the "second" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP increased 3.7 percent.Positive Contributions

The GDP estimates released today are based on more complete source data than were available for the "advance" estimate issued last month. In the advance estimate, the increase in real GDP was 2.4 percent (see "Revisions" on page 3).

The increase in real GDP in the second quarter primarily reflected positive contributions from nonresidential fixed investment, personal consumption expenditures, exports, federal government spending, private inventory investment, and residential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.

The deceleration in real GDP in the second quarter primarily reflected a sharp acceleration in imports and a sharp deceleration in private inventory investment that were partly offset by an upturn in residential fixed investment, an acceleration in nonresidential fixed investment, an upturn in state and local government spending, and an acceleration in federal government spending.

Real personal consumption expenditures increased 2.0 percent in the second quarter, compared with an increase of 1.9 percent in the first. Real nonresidential fixed investment increased 17.6 percent, compared with an increase of 7.8 percent. Nonresidential structures increased 0.4 percent, in contrast to a decrease of 17.8 percent. Equipment and software increased 24.9 percent, compared with an increase of 20.4 percent. Real residential fixed investment increased 27.2 percent, in contrast to a decrease of 12.3 percent.

The change in real private inventories added 0.63 percentage point to the second-quarter change in real GDP, after adding 2.64 percentage points to the first-quarter change. Private businesses increased inventories $63.2 billion in the second quarter, following an increase of $44.1 billion in the first quarter and a decrease of $36.7 billion in the fourth.

- Nonresidential fixed investment increased 17.6 percent

- Personal consumption expenditures increased 2.0 percent

- Real residential fixed investment increased 27.2 percent

- Equipment and software increased 24.9 percent

- Real private inventories added 0.63 percentage point to the second-quarter change in real GDP

Take a look at that list and ask "How many of them will increase again in Q3?" Any?

Amazingly, the deceleration in second quarter GDP was "partly offset by an upturn in residential fixed investment, an acceleration in nonresidential fixed investment, an upturn in state and local government spending, and an acceleration in federal government spending."

Think housing will add to GDP in Q3? State and local government spending?

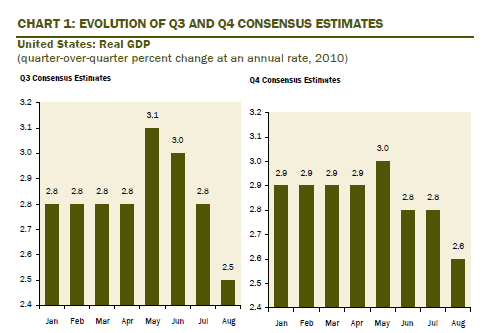

Evolution of Estimates

Dave Rosenberg discusses GDP in today's Breakfast with Dave.

REVISIONISTS UNITE!Treasuries Hammered

Like the equity analysts, the economists are now in the process of cutting their GDP forecasts — but in dribs and drabs, and nothing very draconian just yet. It is interesting to see that the hopes of a 3%-plus growth for this quarter have been marked down to 2.5% in just three short months and frankly, it looks like the economy may even be contracting right now. The consensus has only now begun to touch Q4, and there is probably much more work to do on this score as well.

The bright light in the Q2 revision was the uptick to consumer spending, to a 2% annual rate from 1.6%, while at the same time we had the inventory line revised lower to a $63.2 billion build from $75.7 billion. This configuration is alleviating concerns that a move to take inventories down in the third quarter will be necessary since household spending held up better than earlier expected.

Real GDP in the U.S. came in higher than expected, coming in at 1.6% versus market expectations of 1.4% in Q2. Boy oh boy, 1.6% never felt so good. Be that as it may, much of the upward revision on consumer spending was in services and non-durables, and it looks to be energy related (gas, electricity). In real terms, consumption of gasoline/other energy goods rose at a 4.7% annual rate whereas in the previous “take” on Q2 GDP it was reported to be up only at a 0.7% annual rate. Spending on utilities also swung from what was reported before as a 0.7% decline to a 1.5% increase. Strip out the energy components, and consumer spending did not improve at all from the last Q2 report we were issued a month ago. In other words, if not for the fact that more of the household budget was diverted to the energy bill in Q2, consumer spending would have shown a 1.6% growth rate and GDP would have actually come in BELOW consensus, at +1.3%. Notably, consumer spending on big-ticket durable goods came in lower than initially estimated — trimmed to a 6.9% annual rate from 7.5%.

Here’s what is important to take away:

- We had 5% real GDP growth in the fourth quarter of last year, followed by 3.7% in Q1, 1.6% in Q2 and now what looks to be little better than 0% this quarter. So the notion that the economy has hit stall speed has not changed in this report —if anything, it was enhanced.

- Real final sales — GDP excluding inventories — was actually marked down in this report to a meager 1% annual rate. That is really soft and underscores the overall weakness in the demand guts of the economy. We know from the monthly data that much of this paltry 1.6% growth in Q2 was baked into April — four months ago! — and that the pace of activity has weakened markedly ever since.

- The monthly GDP data have actually shown declines for two months running and there is a negative “build in” so far for Q3. There is practically no growth in real consumer spending heading into the current quarter and we know that back-to-school sales so far have been sluggish.

One more comment on Q2 — just to put 1.6% into context. Historically, four quarters following a bottom in GDP, growth is running over a 6% annual rate. Rejoicing over 1.6% because it wasn’t 1.4%, particularly in the context of the most radical bailout, monetary and fiscal stimulus in U.S. history, totally misses the point that we are operating in a totally abnormal and fragile economic environment.

After a massive rally in treasuries since April, at some point there was bound to be a correction. Exciting news of an unexpectedly "good" GDP at 1.6% was a nice trigger.

The selloff looks sharp but it's not. 10-year treasury yields were above 4% in April. The 10-year yield after today's hammering is 2.64%.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List