A Major Disconnect

Mish Moved to MishTalk.Com Click to Visit.

Mish Note: I wrote this last week and it was originally published by Whiskey&Gunpowder last Friday. The charts are slightly out of date (from the 25th), but in reality not much has changed since I wrote it. The important message is the conversation I detail below, especially the ideas presented by Minyanville professor Scott Reamer. Please listen to what Scott has to say. Here goes:

There was an interesting conversation on Minyanville on September 26th between Kevin Depew and Scott Reamer. Let's tune in.

Kevin Depew:

"You guys always seem bearish," someone wrote me last night. That's simply not true.

Frankly, it is extraordinarily difficult to make money betting against stocks. And I don't know of any Professors at Minyanville who are permanently bearish. If Minyanville seems bearish it's just by comparison to the always-bullish-all-the-time news that permeates the mainstream media that it just seems that way.

So far this morning all I've read are bullish stories. Everything is bullish. Here are some of the bullish things I've read this morning:

- The decline in oil and gasoline prices is bullish because it helps the low-end consumer.

- The rise in oil and gasoline prices, if it happens, is bullish. It shows good economic growth.

- The price wars over generic drugs is bullish because it helps free up discretionary income for those retirees who tend to spend the most money on prescriptions.

- The declining housing market is bullish because it dampens inflation and makes housing more affordable.

- The "unexpected" recovery in the housing market, if it happens, is bullish because it furthers the "wealth effect."

- Rising rates are bullish because that signals strong economic growth.

- Falling rates are bullish because that helps drive mortgage refinancing and cushions ARM resets. A falling dollar is bullish because it makes exports more attractive.

- A rising dollar is bullish because it makes imports less expensive.

Data itself doesn't matter. It's the environment into which it is fed that matters. In this case, since we are seeing historic, record risk-seeking (bullishness/complacency) EVERYTHING is bullish or considered so. So ANYTHING people say or data that comes in - even the most bearish (like housing stuff or UPS, LEND, HRB etc) - is "bullish" because people are in that frame of mind. It's at such an extreme and it is THAT condition that appears to be nearing an important - critical - inflection point.

Of course, both lower and higher oil prices cannot be bullish together. Understanding that particular riddle comes from understanding that it isn't the DATA itself that matters - but the psychological environment into which it is fed that matters. And THAT is the environment which you should be trying to measure and analyze. Not the data.

Mish:

When everything is bullish or everything is bearish you have the makings of a major disconnect. But context is important too. When stocks no longer fall on bad news or when stocks stop rising on good news a major turning point is often at hand. At such turning points the market will typically lead the data, sometimes by months. In the current situation stocks have been pretty much rising for three months on about any news. Had this happened after an enormous decline or deep into a recession it would likely be signaling a reversal.

We have now gone three years without so much as a 10% downward correction in the S&P. Although the markets may be signaling something, what exactly is it? Is this a replay of the 1994 goldilocks scenario? Looking at the stock market in isolation one might easily arrive at that conclusion. A look at treasuries, commodities, the relative performance of the S&P vs. the Russell Smallcaps, and a look at the DOW vs. the DOW Transports paints a different picture. Let's look at some of the concurrent data.

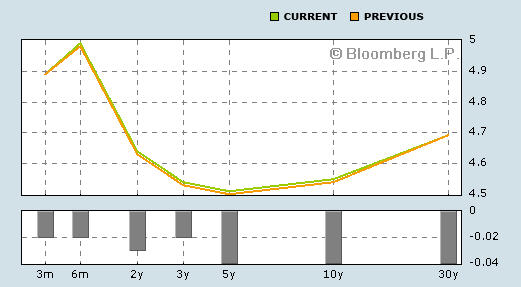

Yield Curve

Here is the yield curve as of 2006-09-25

Currently there is a 67 basis point spread between the Fed Funds rate and the 10 year treasury. That is a quite steep inversion and one in which lenders should have trouble borrowing short and lending long, especially on mortgages.

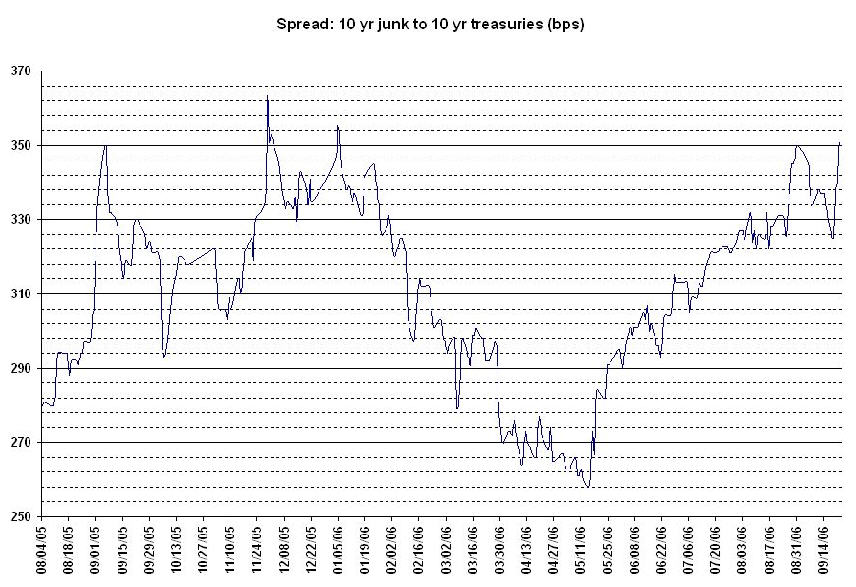

Here is a chart of junk bonds spreads vs. treasuries.

The above chart was produced by Orkrious on Silicon Investor who plots the data every day. As you can see, credit spreads have been widening since May. That is typically a sign of stress (at least in the long term presuming the trend continues). Such a trend is generally not good for stocks (to put it mildly).

Please consider the DOW vs. the DOW Transports.

DOW

Transports

The DOW is about to make a new multi-year high while Transports are nowhere close.

In DOW theory that is a bearish divergence.

Homebuilders

Remarkable complacency is being shown in warning after warning after warning from homebuilders. At least with homebuilders one might have expected a snapback rally based on sentiment. Indeed bears had a warning when the builders stopped falling on bad news. But homebuilders rising for months on repeatedly bad news sure seems like another disconnect.

Check out Lennar's Third Quarter Lennar Reports Third Quarter EPS of $1.30

Financial Highlights

- Revenues of $4.2 billion - up 20%

- EPS of $1.30 - down 37%

- Gross margin on home sales of 18.7% - down 760 basis points

- Gross profit on land sales of ($0.3) million - down $46.7 million

- Financial Services operating earnings of $61.7 million - up $26.8 million

- Homebuilding debt to total capital of 31.9% - 520 basis point improvement

- Return on equity of 25.2%

- Deliveries of 13,038 homes - up 19%

- New orders of 11,056 homes - down 5%

- Gross margins are down 760 basis points to 18.7%. That is a staggering decline.

- Gross profit on land sales is now negative. Lennar is unloading land and/or options which shows lack of confidence going forward.

- Financial Services Operating Earnings had a 77% increase (from 34.9 to 61.7). To what extent is Lennar taking on risk (keeping the loans) just to unload houses?

Let's now consider the pool business.

Reuters is reporting Pentair cuts profit forecast on weak pool business

Saying that weakness in the housing market was taking a toll on its swimming pool equipment business, diversified manufacturer Pentair Inc. (PNR) on Tuesday cut its earnings outlook for the third quarter and full year, and said it was taking steps to cut costs.Enquiring minds might be wondering about home improvements. MarketWatch is reporting Lowe's cuts profit estimate to lower end of forecast

Pentair, which also makes fluid-handling systems and industrial products, said it would earn between 30 cents and 32 cents per share in the third quarter, including a charge of about $17 million, down from its previous estimate of 46 cents to 50 cents.

Pentair also lowered fourth-quarter guidance to a range of 33 cents to 35 cents from 53 cents to 59 cents, resulting in full-year guidance from continuing operations at $1.72 to $1.76 a share. Analysts polled by Reuters Research predicted $2.07 per share for the year.

"This adjustment reflects the effect of the housing slowdown on spa and bath markets and on new pool starts," said Randall Hogan, Pentair chairman and chief executive officer.

Pentair said Charles Brown had stepped down as president and chief operating officer of its Pump and Pool & Spa units.

Home-improvement-goods retailer Lowe's Cos. said it now expects profit for the year that's toward the lower end of its prior view, citing consumer pressures such as a lackluster housing market and high energy costs, and it conceded Tuesday that it expects weakness to continue into next year.Generally a second warning or miss is a kiss of death but Lowe's rose slightly today. While Wachovia believes (as do I) "there is no sign of the housing market reaching a bottom", for now anyway, the market simply does not care. More interesting to me is the comment by Goldman: "We expect aggressive expenses control." Aggressive expense control huh? How many layoffs are we talking about anyway?

In a Tuesday presentation to analysts and investors, Chief Financial Officer Robert Hull said he's seen the home-improvement customer pull back over the last few months, but the company has been looking into other high-margin growth areas as a way to boost profit and gain market share.

The slowdown in the housing market has been a concern for home-improvement retailers. They'd been ringing up robust sales in recent years as a booming real-estate market and low interest rates encouraged consumers to refinance mortgages or take out home-equity lines of credit to remodel. Competition from rival Home Depot Inc. and regional players has also intensified.

Last month, Lowe's shares fell after the retailer reported second-quarter earnings that missed Wall Street's outlook. At that time, Lowe's also cut its full-year profit forecast, citing pressure on consumer spending from higher energy prices and a slowing housing market.

Goldman Sachs analyst Matthew Fassler wrote in a note to clients. "Management's earnings guidance in the midst of flagging sales is credible. ... Moreover, we expect aggressive expenses control."

[Peter Benedict, Wachovia stated] "We believe there is still risk that more estimate reductions are ahead given there is no sign of the housing market reaching a bottom."

Speaking of layoffs, Haver is reporting Mass Layoffs Up.

September 21, 2006

- In August, the number of mass layoff events rose for the third consecutive month. The 6.0% m/m increase pulled the y/y comparison positive for the first time since December.

- During the last ten years there has been a (negative) 85% correlation between the three month average level of layoff announcements and the y/y change in payroll employment.

- The number of persons affected last month by mass layoffs surged 11.4% m/m but were up just 0.3% y/y. The number of persons affected by mass layoffs during the first eight months of this year fell 12.6% from the first eight months of 2005.

- Increased layoffs in manufacturing (21.2% y/y) and information (-35.0% y/y) dominated the increase in claimants for unemployment insurance last month. Declines elsewhere were widespread.

- Mass layoffs are heading back up after falling for quite some time.

- The 85% correlation suggests unemployment will rise

- Layoffs were in manufacturing and information.

- Housing and retail related layoffs are not part of the picture, not YET anyway.

- A hugely inverted yield curve is suggesting a recession

- Mass Layoffs are increasing

- Unemployment is expected to rise

- Home builder margins are rapidly shrinking

- Everything related to housing seems toxic

- Credit spreads are widening

- Commodities are dropping

- Bankruptcies and foreclosures are rising

- "We are seeing historic, record risk-seeking (bullishness/complacency) where EVERYTHING is bullish or considered so." (Mish note: except for commodity prices themselves and commodity related stocks).

- The stock market is priced for a "Goldilocks" scenario, if not better.

- There is obviously a major disconnect here.

- The resolution is guaranteed to be interesting.

- In the meantime, hiding out in short term treasuries is a very good looking alternative.

http://globaleconomicanalysis.blogspot.com/