Lending Guidelines / Credit Squeeze

Mish Moved to MishTalk.Com Click to Visit.

The Federal Reserve came out today with new 27 page PDF of Lending guidelines. Here is the gist of it.

The Agencies developed this guidance to address risks associated with the growing use of mortgage products that allow borrowers to defer payment of principal and, sometimes, interest. These products, referred to variously as “nontraditional,” “alternative,” or “exotic” mortgage loans (hereinafter referred to as nontraditional mortgage loans), include “interest-only” mortgages and “payment option” adjustable-rate mortgages. These products allow borrowers to exchange lower payments during an initial period for higher payments during a later amortization period.Ramsey Su on Silicon Investor offered this analysis

While similar products have been available for many years, the number of institutions offering them has expanded rapidly. At the same time, these products are offered to a wider spectrum of borrowers who may not otherwise qualify for more traditional mortgages. The Agencies are concerned that some borrowers may not fully understand the risks of these products. While many of these risks exist in other adjustable-rate mortgage products, the Agencies’ concern is elevated with nontraditional products because of the lack of principal amortization and potential for negative amortization. In addition, institutions are increasingly combining these loans with other features that may compound risk. These features include simultaneous second-lien mortgages and the use of reduced documentation in evaluating an applicant’s creditworthiness.

The Agencies proposed that for all nontraditional mortgage products, the analysis of borrowers’ repayment capacity should include an evaluation of their ability to repay the debt by final maturity at the fully indexed rate, assuming a fully amortizing repayment schedule. In addition, the proposed guidance stated that for products that permit negative amortization, the repayment analysis should include the initial loan amount plus any balance increase that may accrue from negative amortization. The amount of the balance increase is tied to the initial terms of the loan and estimated assuming the borrower makes only the minimum payment.

The Agencies believe that institutions should maintain qualification standards that include a credible analysis of a borrower’s capacity to repay the full amount of credit that may be extended. That analysis should consider both principal and interest at the fully indexed rate. Using discounted payments in the qualification process limits the ability of borrowers to demonstrate sufficient capacity to repay under the terms of the loan. Therefore, the proposed general guideline of qualifying borrowers at the fully indexed rate, assuming a fully amortizing payment, including potential negative amortization amounts, remains in the final guidance.

Furthermore, the analysis of repayment capacity should avoid over-reliance on credit scores as a substitute for income verification in the underwriting process. The higher a loan’s credit risk, either from loan features or borrower characteristics, the more important it is to verify the borrower’s income, assets, and outstanding liabilities.

Immediate Reaction:

- If the guidelines are followed, which I don't know how they can not follow, a ton of loans in the pipeline are going to be rejected. Furthermore, the recasters are going to have hell of a time refinancing, while the existing loans are all going to be non-conforming to these guidelines.

- The big question is applicability to the non regulated lenders such as NEW, LEND and NFI. Could they actually benefit because all the regulated lenders such as CFC, WM, WFC would all be forced out of the market. I find it hard to believe that the powerful banking lobbyist would allow that to happen so it would be only short term.

- I think it has teeth because while they are just guidelines, the banks are going to have to explain to the examiners why they choose to ignore the guidelines if they continue to lend using old underwriting standards. They guidelines are pretty clear.

The Fraud Prevention Coalition, a national alliance of companies formed for the advancement of tools to prevent mortgage fraud, announced the Internal Revenue Service (IRS) has completed the development of a system providing secure electronic return of tax transcripts. The new "Express Service" is expected to take effect Oct. 1, 2006, and includes electronic transcripts of personal and business tax returns that will be made available significantly faster than the current two-day program it is replacing. Additionally, W2s, 1099s and K1s will be added to the program within thirty to sixty days.Fib Spotting

Income verification is a tool used by mortgage lenders and others within the financial community to confirm the income of a borrower at the beginning of the loan application process in an efficient and cost effective manner. Verifying income via tax transcripts provided by the IRS can detect potential fraud and reduce the risk of repurchase demands.

The Hartford Courant is reporting Lenders Will Be Spotting Income Fibs Much Faster.

October 1, 2006Credit Squeeze

Starting Monday, it's going to get much riskier to fib about your income when you apply for a home mortgage. That's because the Internal Revenue Service is overhauling a key income verification tool used by lenders - making it faster and easier to pull up electronically the confidential income tax information of borrowers.

"It could be huge" in spotting fraud upfront - before it's too late - said Mike Summers, vice president of Veri-tax.com, a Tustin, Calif.-based firm that services 3,000-plus large and small mortgage lenders nationwide. Fraud in mortgage applications is now a multibillion-dollar-a-year problem, according to the FBI, and falsified income tax filings are an important contributing factor.

Some popular mortgage products themselves open the door to bogus assertions about income. Many lenders in recent years have offered "stated income" and other limited documentation mortgages aimed especially at self-employed applicants. Dubbed "liar loans" by industry critics, stated-income mortgage programs allow applicants to bypass standard underwriting requirements for W-2s or copies of personal and corporate income tax records.

Instead, applicants simply assure the loan officer or broker that, yes indeed, we earn enough to qualify for the mortgage, and the transaction proceeds to closing.

Often lenders will ask borrowers to fill out what is known as an IRS Form 4506-T along with their other mortgage documents.

That form authorizes the lender or the investor providing the money for the mortgage to obtain transcripts from the IRS summarizing income and tax data for as many as four years. The form must be signed by the borrower and can be used only during the 60-day period after the date of signing.

Until now, the process of faxing in 4506-T requests to the IRS and obtaining transcripts has been paper-driven and non-electronic - making income verifications slow and difficult to fit into lenders' highly automated loan underwriting systems. Most lenders have used 4506-T forms as a way to perform quality-control checks on pools of closed mortgages.

The only downside from a lending industry perspective: Rather than providing transcripts at no cost, as in the past, the IRS now plans to charge a flat $4.50 for each tax year covered in a 4506-T request.

Typically lenders want to see two years of returns, so the IRS's policy change means that costs will jump by $9 per loan application.

The Christian Science Monitor is reporting Risky mortgages threaten a squeeze

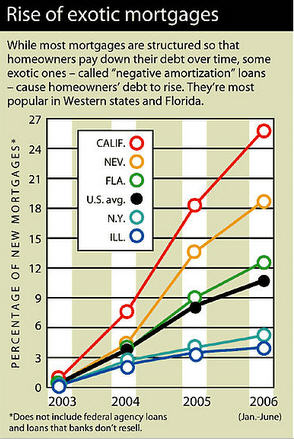

In 1990, the last time the nation was entering a real estate slowdown, less than 10 percent of home loans were ARMs, adjustable-rate mortgages. For the first half of this year, that number is 46 percent of the total, measured in dollar volume, says Richard Brown, chief economist at the Federal Deposit Insurance Corp.On a national basis 46% of loans in 2006 were adjustable and of those 63% were non-traditional. In other words 29% of all loans nationally were either interest only or pay option arms. That is likely to be a huge problem as interest rates reset. The chart above shows the number of neg-am loans. It is close to a staggering 27% of all loans this year in California. If the only way people could "afford" those homes was the low teaser rate, then look for a huge drop in purchases as the lending guidelines are followed.

Of all the adjustable-rate loans, 63 percent of them this year have been nontraditional: either "interest only" loans (it's up to the buyer whether to pay any principal to build home equity) or "option ARMs," which give borrowers a choice of several possible payments each month. Even fixed-rate loans today can be "interest only."

The biggest trouble lies with the adjustable loans that begin with artificially low interest rates. Those rates may only last for a month, a year, or two years, and then comes a "payment shock" as the rates reset in ways that can double the required payments.

Earlier this year, an analysis by First American Real Estate Solutions in Santa Ana, Calif., estimated that $368 billion in adjustable-rate mortgages originated in 2004 and 2005 are at risk of default because of this pattern. Many more borrowers with traditional ARM loans also face the prospect of rising interest rates, but of a more manageable magnitude.

"This translates into ... 1.8 million families that are at risk as a result of the possibility of default and another 500,000 that are likely to go into foreclosure," Allen Fishbein of the Consumer Federation of America said last week at a Senate hearing on nontraditional mortgages.

Who is most at risk? Exotic loans have been rising nationwide, but are most prevalent in states such as California, Nevada, and Florida where home prices have been rising fastest. They are far less common in the Northeast or Midwest.

"It will take more than five years to get housing valuations back to where they ought to be," Merrill Lynch economist Sheryl King writes in a recent report.

"It's a time release," says Christopher Cagan, who did the risk analysis at First American Real Estate Solutions. "It's not a single impact like Pearl Harbor."

Summary of Effects

- Stated income loans all but vanish

- Pay option arms all but vanish

- Pool of eligible buyers shrinks

- Inventories will rise

- Increased downward pressure on prices

- California, Nevada, Florida hardest hit

- Foreclosures will continue to rise

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/