The Kondratieff Cycle Revisited

Mish Moved to MishTalk.Com Click to Visit.

Deflationists argue, "Next year, in America!"

They have been wrong every year since 1933.

Inflationists argue, "Next year, in America!"

They have been correct every year since 1933.

Gentlemen, place your bets!

Those are the arguments Gary North presented in Inflation vs. Deflation Revisited.

Monetary inflation produces price inflation.

Monetary deflation produces price deflation.

The most important money supply charts are found here.

I implore you: click this link. http://snipurl.com/fedcharts

Click the first three links on the page.

If you refuse to do this, then you are not really

interested in the inflation vs. deflation debate.

Several days later Gary North argues Price Deflation: A Great Idea With Low Probability.

North states: "You will find a statistic that the deflationists are either unaware of or prefer that their subscribers remain unaware of. Fact: in not one year since 1992 has the rate of price deflation in Japan fallen by as much as 1%. In half of the years, Japan experienced price inflation. In 2004, prices were flat.

What does this tell us? It tells us that the deflationists have neither economic theory nor modern economic history on their side. They are really lousy psychologists, too."

To those articles let me briefly respond:

I agree with North using Japan as the model since that is the model deflationists use. However, if inflation is the expanse of money and credit, then deflation is the opposite. "Price Deflation" muddies the argument. There are reasons that prices could be falling that have nothing to do with deflation (productivity or huge harvest) and there are reasons prices could be rising that have noting to do with inflation (peak oil or supply disruptions or weather).

The heart of the matter was a collapse of CREDIT that actually overwhelmed Japan even as the central bank tried to prevent it by injections of money. That collapse in credit caused Japan's mammoth asset bubbles to pop and housing prices to decline 18 straight years. It also caused the stock market to fall from 40,000 to 7,000 or so in the same time. North ignores declining credit for 60 straight months even as the Bank of Japan tried to prop things up via money supply.

What about prices in Japan?

Ojisan on the Motley FOOL writes: I lived in Japan from 1997-2000, and prices of many good and services definitely fell, including food items, haircuts, movie tickets, travel, subscriptions, etc.

With services, most of the time it was difficult to see deflation from the outside because the listed prices didn't change much, but discounts and "specials" became so common that getting less than the actual price was easy. In the case of subscriptions, for example, companies started throwing in freebies, like coupons for other stuff, household goods, etc., so the consumer was getting more for the same Yen.

Of course, durable goods fell in price, but that's pretty much expected, especially on the tech side. Still, 100-yen shops (dollar stores) sprung up all over the place while I was there, with some pretty surprising stuff, most of it made in Korea, China, and Malaysia. Second hand shops, previously shunned by Japanese, became more popular, and more common, putting pressure on department stores, forcing constant sales.

Finally, it became noticeable easier to haggle, even in the dept. stores. When I bought a video camera, for example, they threw in all kinds of extras to close the deal. So, technically, I paid the listed price, but not really.

Ojisan

Is it that unlikely that with rising unemployment in the wake of a housing crash that prices of movies, haircuts, and other services drops here too? I think not. If inflationists point out rising home prices as evidence of inflation, then they must point out home price declines as evidence of deflation if and when a housing bust happens.

Inflation Monster Captured

Following is a snip about deflation in Japan from Inflation Monster Captured

There are many that think true deflation (decrease in money supply) can not happen under a fiat system. I disagree but perhaps the point is moot. Money supply itself actually never contracted in Japan. Instead, it grew very slowly for quite some time. However, bank credit outstanding contracted for 60 months in a row. Clearly there was a credit contraction. How did money supply still manage to grow? Fiscal deficits were ramped up immensely, roads to nowhere were built, and the Bank of Japan monetized all of it.As for current monetary conditions, the entire Mx (M1, M2, M3, MZM) monetary series is known to have double counting errors. In addition, the Mx series fails to properly distinguish between credit and money. Frank Shostak pointed out these flaws out in an article about Austrian Money Supply (Money AMS) entitled Making Sense of Money Supply Data.

In addition, money velocity plummeted. The net effect of the credit contraction on prices was clearly what one would nowadays call "deflationary". Prices across a broad range of assets and goods and services fell. Indeed, practically everything fell but government bonds. People were amazed at the alleged "bond bubble" as well as the Zero Interest Rate Policy (ZIRP) of the BOJ. However, a 1% interest rate on a 10-year bond makes sense when prices fall 2.5% annually. The real yield is obviously far higher than 1%. Perhaps a practical way to think of deflation under a FIAT system is the destruction of credit/debt that exceeds growth in money supply.

Current money supply (Money AMS) figures are much tighter than meets the eye. A glance at the yield curve suggests the same thing.

Five problems in dismissing the deflation argument:

- Projecting forever into the future the inflation one sees today

- Failure to understand the deflationary nature of a credit implosion

- Failure to understand the magnitude of the credit implosion that is likely to come with a housing bust

- Failure to understand the difference between money and credit and how credit collapsed in Japan even as the BOJ attempted to fight it

- Assuming that deflation in Japan was a cultural thing and can not happen here

In Bernankeism: Another Good Reason To Buy Gold Jay Taylor writes:

"There is no means of avoiding the final collapse of a boom brought about by credit (debt) expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit (debt) expansion, or later as a final and total catastrophe of the currency system involved." - Ludwig von MisesThe K-Cycle: Myth or Reality?

Sooner or later? That is the question. I remain convinced that Ian Gordon's Kondratieff winter scenario will come to pass. Then we will see massive bankruptcies, enormous levels of unemployment, extremely high rates of savings and debt repudiation, and the excesses of the economic slate will be wiped clean and a new K-cycle can begin. That will be a horrible environment for commodities but not for gold and cash.

Is the whole idea of the Kondratieff Cycle just a figment of some very imaginative minds?

In The Kondratieff Cycle: Real or Fabricated? Murray N. Rothbard writes:

One of the worst things about the "business cycle" is its name. For somehow the name "cycle" caught on, with its implication that the wave-like movement of business is strictly periodic, like the cycles of astronomy or biology. An enormous amount of error would have been avoided if economists had simply used the term "business fluctuations." The fact is, however, that these waves are in no sense periodic; The periodic notion was unfortunately fed by the fact that the early panics seemed to be ten years apart: 1837, 1847, 1857, but pretty soon that periodicity broke down.Objections to the K-Cycle

One of the mystical "cycles" that has been getting a lot of play from time to time is the flimsiest "cycle" of them all: the Kondratieff long cycle. The Kondratieff is supposed to be a strictly, or at least roughly, periodic cycle of about 54 years, which allegedly underlies and dominates the genuine cycles for which we have actual data. Even though, as we shall see, this cycle is strictly a figment of its fevered adherents' imagination, there does seem to be some sort of cycle in the periods when the "Kondratieff" captures the interest of financial and economic analysts.

Most of the Kondratieffites confidently predicted that the peak would arrive in 1974, just 54 years after the previous peak. Previous peak-to-peak stretches had been 52 (from 1814 to 1866), and 54 (1866 to 1920). So where indeed is the peak? It is now 1984 and counting. We are ten years past the confident prediction and we still have inflation. The Kondratieffites have been forecasting imminent deflation since the magic 1974 year, but still . . . nothing!

Time is inevitably running out on the Kondratieffites. For there will be no Big Bang, no repeat of 1929. Pointing to problems in the economy, to stagnation, to stagflation, to falling commodity prices, to secular rises in the unemployment rate, while interesting and significant is not enough. It does not demonstrate the Kondratieff. After all, there are always economic problems. The point is that there is no permanent depression, and there is not, and will not be, any deflation. The idea that we are right now in the midst of a Kondratieff depression, but that the deflation is being masked by inflationary bank credit, cannot be the way out. For that is simply the mystic's fudge factor so that you can never prove him wrong, regardless of the evidence. No, the Kondratieff is dead, and now it is simply a question of how long it will take the Kondratieffites to lie down, to admit defeat and slip away into the night.

We can only sum up the correct answer to the problem of the business cycle. We have already seen a hint of the solution: that inflation and the inflationary boom are caused by bank credit expansion generated by governments. In fact, government's central banking system provides the key causal element for all business cycles, a cause exogenous to the market economy. Continuing government intervention sets in motion business cycles by generating inflationary booms. Because these booms distort the signals of the market place in interest rates and in relative prices they bring about grave distortions of production and prices, which must be corrected by recessions and depressions.

And so we see – and this is the great insight of the "Austrian" theory of the trade cycle – that micro and macro economics are in harmony after all. The free market does tend to adjust harmoniously without boom and bust, without incurring clusters of severe business losses. It is government intervention in the market that creates the business cycle, and unfortunately makes the corrective adjustment of recessions necessary. The cause of the boom-bust cycle is not some mystical periodic Force to which man must bend his will; the fault, dear Brutus, is not in our stars but in ourselves, that we are underlings.

In reading the above I believe one can summarize Rothbard's biggest objections as follows:

- The K-Cycle is not governed by nice neat waves at regularly spaced intervals.

- The K-Cycle is not a natural cycle. It is based on government intervention and other outside factors.

- Kondratieffites changed the meaning of the word "depression" as needed to curve fit 54-year cycles.

Is "cycle" even the right name? Would "business fluctuation" be better? Then again: "What’s in a name? That which we call a rose by any other name would smell as sweet."

The Chinese have a much simpler way of looking at things: "Three generations rich, fourth generation poor." I am sure as far as generalities go that one is as good or as bad as any other, but the implications seem obvious enough: People forget that prosperity is a result of hard work and saving. Far enough removed, no one remembers the previous economic bust nor do they think there will ever be another one.

Sticking to fixed cycles of 54 years led to many premature K-Winter calls by various people, some of them being rather famous. But does that mean there will not be an upcoming bust simply because it has not happened in the prerequisite time frame? That we will have another bust as a result of the reckless over expansion of credit seems to be an Austrian given. A rise from those ashes also seems relatively assured.

Let's study the following paragraph in greater detail:

The point is that there is no permanent depression, and there is not, and will not be, any deflation. The idea that we are right now in the midst of a Kondratieff depression, but that the deflation is being masked by inflationary bank credit, cannot be the way out. For that is simply the mystic's fudge factor so that you can never prove him wrong, regardless of the evidence. No, the Kondratieff is dead, and now it is simply a question of how long it will take the Kondratieffites to lie down, to admit defeat and slip away into the night.

I am not aware of any K-Cycle theorists calling for a "permanent depression", and if there are some that suggested we were in the midst of a Kondratieff depression in the 80's or 90's they were most certainly wrong. As for fudge factors: Is there much difference between believing in the inevitability of K-Winter vs. the inevitability of a "final collapse of a boom brought about by credit (debt) expansion"? If so, what is that difference? That said, the valid objections of Rothbard as pertaining to the various 54 year "cycles" as they have been labeled on various Kondratiev Charts should indeed more that raise a few eyebrows.

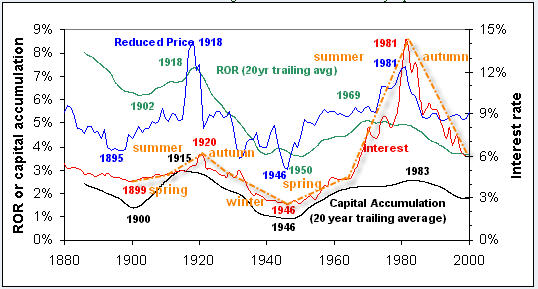

K-Cycle Theory:

- There is inflation (reflation) in Spring.

- There is inflation (rapidly rising interest rates) in Summer.

- There is inflation (although at a declining rate) in Autumn.

- There is deflation in Winter.

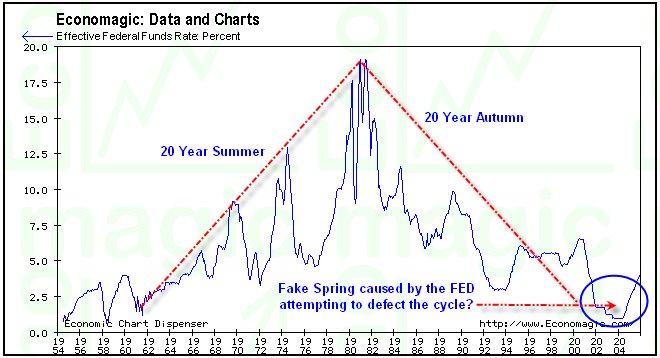

Following is an "Interest Rate Interpretation" of the K-Cycle

Here is a longer term view:

Are the above charts "curve fitting"? Regardless, why should anyone subscribing to cycle duration methodology have expected deflation to begin in 1984 or even 1994 for that matter?

Consider once again Ludwig von Mises "There is no means of avoiding the final collapse of a boom brought about by credit (debt) expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit (debt) expansion, or later as a final and total catastrophe of the currency system involved."

The implication is that cycles are not about a fixed period of time per se, but rather the concept that malinvestments during the boom years will be repudiated (voluntarily or not) in a collapse in credit (debt) during K-Winter. Perhaps the cycles are getting longer. Mises statement would seem to allow it. There are by the way two possible explanations for why the cycles seem to have lengthened. For one thing, people live longer than they used to. These days, three generations tend to simply last longer than during the last K-cycle iteration. The other reason is that central banks have become 'better' at co-ordinated intervention. In short, they tend to intervene sooner, and with more firepower, at the first hint of recession. They are deathly afraid that the debt-berg could implode and kick off the 'winter', deflation and all. The problem is, they can't really avert its arrival, but they sure can delay it, and make the ultimate resolution worse in the process.

With those ideas in mind, consider the following chart.

Another Deflationist Excuse?

I propose what we have really seen since the 2002 lows is a "False Spring" reflation caused by the FED slicing interest rates to 1% in a foolish attempt to defeat the current cycle. That intervention created an echo bubble in housing and an even bigger bubble in credit expansion. The reason that it was a "False Spring" is the excesses of the previous credit expansion have never been purged. Consumers never stopped spending and instead went deeper in debt.

Were those touting deflation in 2000 wrong yet again? If so, was this yet another case of Kondratieffites "fudging excuses" as Rothbard might have suggested or was it more like "prolonging the agony" to paraphrase Ludwig von Mises? I suggest both may be correct depending upon whether or not one is trying to force fit a rigid 54 year cycle on a chart that makes little sense as opposed to believing that repudiation of debt is a cyclic phenomenon that happens in K-Winter regardless of how long each cycle is. At any rate, it seems that no one sees deflation, or even a recession as likely now. There is even talk from Greenspan that "An inverted yield curve does not mean what it used to". At the peak of every boom "It's different this time" type of arguments abound.

Here is the Deflation Case once again:

- Rising productivity and rampant credit expansion led to massive overcapacity.

- Global wage arbitrage is putting downward pressure on wages and benefits.

- An enormous bubble in credit lending developed causing malinvestments and speculation.

- Speculative credit lending fueled bubble prices in houses and other assets including the stock market

- At some point housing prices will fall as the pool of stupid buyers exhausts itself. The housing sector will stall

- A stalled housing sector will cause rising unemployment and lower demand for goods and services, appliances, eating out, etc, etc, etc.

- Bankruptcies will rise.

- Banks will not be willing to extend further credit on assets declining in value, especially to those out of work, or nearly underwater on their homes. In fact, appraisals get tighter at long last.

- Credit lending plunges. We have already seen the second consecutive month of declining consumer credit. This is the first time since 1992. There is every reason to believe a reversal is underway. If not now then soon.

- Bankruptcies and falling asset prices and people walking away from mortgage loans is a destruction of credit.

- If credit counted as inflation on the way up, a destruction in credit MUST be counted as deflationary on the way down.

- The destruction in credit, rising bankruptcies, an unwillingness of banks to lend, and a rising propensity for people to save will be greater than any monetary printing by the FED to stop it. That is what happened in Japan and that is what will happen here.

Ludwig von Mises: "Depression is the aftermath of credit expansion." Whether or not one wishes to label that "depression" as "K-Winter", it is coming like night follows day and Austrian economists know it.

Note:

This will be a topic of discussion on my weekly Wednesday podcast on HoweStreet.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/