Has the FED already overshot?

Mish Moved to MishTalk.Com Click to Visit.

Mish notes:

This post is a revised listing.

The only change is substituting a Bloomberg yield chart for one from Yahoo.

Several people pointed out errors with the yield curve chart in the original post.

The chart from Bloomberg better shows the current inversion and yields.

The fourth chart I maintain in Esignal.

The symbols available are the 13 week, 5 year, 10 year, and 30 year treasuries.

I like that chart because it shows the changes over time.

It seems the 5, 10, and 30 year yields match Bloomberg but the 13 week appears to be the discount at 4.22 instead of the yield which is at 4.32. I have no control over that but mentally make a note that the 13 week should be showing a very slight 4 bps inversion with the 5 year yield in that bottom chart.

Other than the chart switch and the explanations above, there are no other changes.

I am wondering if the FED has already overshot.

With that thought the telepathic bloglines are now ringing off the wall.

Here are a few samples:

- Mish Are you nuts? Inflation is 5%, housing is insane and so are you.

- Mish This is January 14, not April Fools day.

- Mish Look at gold soaring that is signaling inflation.

Let's take a look at a few charts shall we?

Click on any chart for a more readable view.

The above chart is the yield curve as of January 13, 2006.

The two year has now inverted with the three year and the 5 year.

We have been see-sawing across that line for about a month.

A hike in January seems to be a given.

That will put the FF rate above the 6 month, 2 year, 5 year, and 10 year rates.

I suppose we should wait and see but the odds of a hike are about 90% and unless something substantially affects the long end, a clear and substantial inversion is on the way.

Here is a chart of median home prices.

It is no secret that the housing sector has substantially cooled.

Sacramento, Boston, Las Vegas, Washington DC and many bubble areas have dramatically cooled. Inventory is rising practically everywhere.

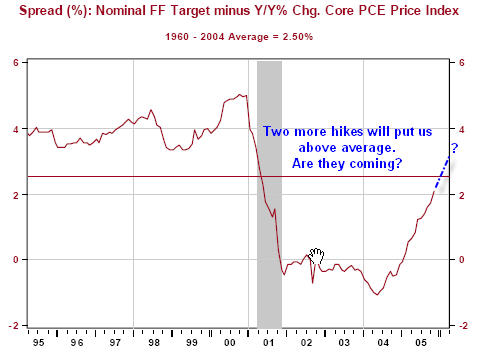

Following is a chart courtesy of Paul Kasriel at the Northern Trust.

The comments in dark blue are mine.

One or two more hiles will put us above the long term trend line.

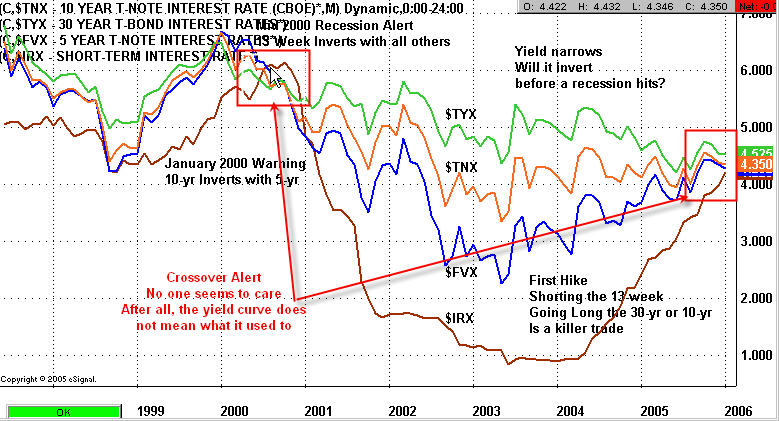

Here is a chart of the 13 week, 5 year, 10 year, and 30 year yields.

Looking at the chart below, one might ask: Is this more like 1999 or 2001?

Given the slope of the 13 week vs the other yields, the duration of this recovery, the slowing of the housing sector, and comments by the FED concerning asset prices, it seems the yield curve is acting more like 2001 and about ready to seriously invert. One or two more hikes with the 10 and 30 holding flat and the chart will look similar to 2001.

Barring some sort of catastrophe that gets the FED to pause, or an inflation scare that causes the long end to rise between now and the end of January, we are going to have a pretty inverted curve vs the flat curve we see today. The equity markets seem to think that the end of the cycle is done. Is it? Will it matter?

For starters it is the nature of the FED to overshoot then over correct. A related thought is that Bernanke wants to prove to the world that he is an "inflation fighter". The concept is totally absurd of course. Everyone knows that but he just may go through the motions and try and prove us all wrong. Thus, from where we are now, there might be not one but two more hikes.

Look at those yield curve charts again. On two more hikes, the 13 week will be yielding more than the 30 year long bond. When that happens it will be interesting to see if the crowd is still chanting "the yield curve does not mean what it used to".

What everyone is missing is the likelihood that the FED has ALREADY overshot. Thirteen hikes with one more a near certainty is a lot of hikes no matter how one looks at it. Interest rates hikes have a very lagging affect and we have not yet fully felt the affects of those hikes already in place. Substantial numbers of mortgage rates will be reset in 2006 and those effects have not been felt. Numerous announced layoffs at GM and other places have not yet been felt. Other than in the refi business, we have not really seen a falloff in housing related jobs. Those are coming too, also with a laging effect. Most of the other risk factors I can think of are negative as well: another oil shock, a blowup of some kind in the Mid-east, a slowdown in China that no one seems to think is possible, consumers saving more, a strike at Delphi, etc etc etc.

The risk is without a doubt dramatically skewed to the downside but every FED governor seems to think otherwise. Sometimes I wonder if they are really speaking their minds. Do they really think this is a strong economy or are they attempting to talk it up in some sort of fairy tale make believe story for some reason?

I keep having this nagging thought that the FED actually knows this recovery is over and furthermore wants to cause a recession. No not a massive slump that will wipe everyone out, but some sort of "mild affair" they THINK they can control. The idea they can control a recession is of course preposterous, but no more so that the FED can engineer a perfect soft landing.

OK Mish why would the FED want to engineer a "soft recession"?

To answer that question, we must take a step back and look at 2001. The thing the FED feared most in 2001 was a complete bust of corporate credit. That is why they slashed rates to 1%. Corporate bonds were on the verge of a complete meltdown. Cash balance sheets of companies were in horrid shape.

Cash balance sheets are in great shape now compared to 2001-2002. The problem is that there are numerous junk bond offerings all for the purpose of share buybacks at absurd prices. Corporations are wasting their cash on buybacks and leveraged buyouts and mergers just as happened in 2000. It seems no one has learned a thing. That is the problem the FED faces and it is not pretty.

To rein in the junk bond bubble the FED may have to futher risk a substantial hit to the housing bubble where a peak is clearly in place. But if the FED allows the junk bond bubble to continue, corporations will continue draining their cash as they did in 2002. If the FED pauses early they give a continued green light to the junk bond market. That is the dilema facing the FED today. The FED must at all costs act to rein in the corporate bond bubble. A "mild recession" hoping to deal with the aftermath may be what the FED is shooting for.

Furthermore, I doubt the FED cares much about consumers or consumer problems until it starts seriosuly affecting corpoarte balance sheets. It's a tough balancing act that is in fact impossible to solve. More than likely the FED has more than overshot when it comes to housing and consumer spending but has not overshot when it comes to popping the junk bond bubble.

Those looking for a bubble in bonds should be looking at the junk bond market not treasuries. Even the junkiest of corporation are having an easy time raising cash for no other purpose than stock buybacks. Literally it is insane and that is one thing the FED is fighting (at least that is what I hope they are doing). So.... Does the FED really think this economy is strong or are they providing an excuse to keep tightening until the junk bond market gets the idea? Am I giving the FED too much credit? Do they really even know what they are doing at all?

If the FED is targeting asset prices, credit lending, and junk bonds, housing might be flattened by the time junk bonds capitulate. Then again there could be some sort of "credit event" as we saw with LTCM where overnight we went from complacency to near panic. The middle ground is to look for two more hikes, followed by a long pause. That is what happened in the UK and we seem to be following in their footsteps. A recession is coming but somehow the junk bond market and the equity markets have not gotten the message or worse yet just do not care (for now). The longer they continue not to care the more potential hikes the FED gets in.

Everything can not be bullish for stock 100% of the time. Stocks were rising as the FED was hiking and the pundits were saying that hikes showed the economy is strong so "buy stocks", now we we are supposed to buy stocks because the fed is about ready to pause. If and when the FED cuts the message will be "buy stocks". No matter what the situation is, the message is constant "buy stocks". Meanwhile the yield curve is saying there is a problem. One more hike with the long end of the curve not rising and the yield curve will be screaming recession. Trust the yield curve.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/