Baby Boomer Time Bombs

Mish Moved to MishTalk.Com Click to Visit.

Warning: This is a very long post, 14 pages or so printed.

It covers 5 aspects of the Boomer Time Bomb. I have been gathering material on this for months and finally decided to write it all up. I tossed out dozens of references that I could have included but then it would have been 40 pages long or so. Some aspects of this are well known, others less so.

In spite of all Bush's hype about Social Security, SS is one of the smaller problems on the list. Social Security is a big problem of course, but closer to now, which of course is all anyone ever worries about these days, is the affect of 10,000 boomers a day retiring starting 2006. More to the point, one has to wonder about promises that have been made to those boomers, and the preparedness (or lack thereof) of many approaching retirement. One also has to consider the demographics looking forward.

The pension problems at GM and Delphi and airlines are widely known but what about state government promises, local government promises? What about cities like San Diego and Duluth that are nearly bankrupt over promises that can not be met? What about states like New Jersey that are borrowing money by selling bonds to fund pension plans then investing that money on the hope and prayer that the stock market will provide adequate returns? What about Illinois? How about silly promises made by the state of Washington? The list goes on and on and on. That is why the following is 14 pages long. I take a look at Social Security, Medicare, Defined Benefit plans, stock market effects, and other savings (or lack thereof).

I talked about The Boomer Time Bomb on my latest podcast with HoweStreet in addition to predictions for 2006. Perhaps some want to tune in to that at http://www.howestreet.com/goldradio/interview.php?audioId=183

This is an important issue and I hope everyone gives due consideration as to how they may be affected by promises that probably can not be kept. Here goes:

Five components to The Baby Boomer Time Bomb

- Social Security

- Medical Expenses

- Defined Benefit Pension Plans

- The Stock Market

- Other Savings

The nation's health care and Social Security system is about to face a rude wakeup call as the first wave of baby boomers retire according to the following highlights from the Social Security and Medicare Boards of Trustees 2005 annual report.

- Annual cash flow deficits are expected to grow rapidly after 2010 as baby boomers begin to retire. The growing deficits will lead to exhaustion in trust fund reserves for Medicare Hospital Insurance (HI) in 2020 and for Social Security in 2041.

- Total Medicare expenditures were $309 billion in 2004 and are expected to increase in future years at a faster pace than either workers' earnings or the economy overall.

- Medicare's annual costs are currently 2.6 percent of GDP, or about 60 percent of Social Security's, they are now projected to surpass Social Security expenditures in 2024 and to be almost twice as great as Social Security by 2079.

- To bring HI into actuarial balance over the next 75 years would require an immediate 107 percent increase in program income or an immediate 48 percent reduction in program outlays or some combination of the two.

- Medicare's financial outlook has deteriorated dramatically over the past five years and is now much worse than Social Security's. This is due primarily to a major change in the projected long-term growth rate of Medicare costs relative to that of the economy and, secondarily, to more rapid expenditure growth so far this decade than previously anticipated. In 2000 annual cash-flow deficits were projected to first appear for HI in 2010. But these deficits actually began last year, resulting in the projected exhaustion date for HI Trust Fund reserves moving forward from 2025 to 2020. HI costs are expected to rise so rapidly thereafter that trust fund income will be adequate to cover only 27 percent of program costs by the end of the 75-year period.

- Expenditures on health care can be expected to rise faster than non-health care expenditures for the foreseeable future. Prudence dictates action sooner rather than later to address the challenges posed by the financial outlook for both Medicare and Social Security.

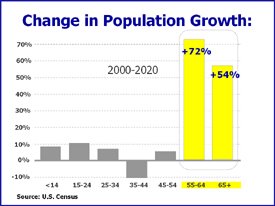

Boomers are turning 50 years old at the rate of 10,000 a day and starting in 2006, the first Boomers will start celebrating their 60th birthdays. There is no looking back.

Healthcare: America's Other Pension Problem

On December 20th BusinessWeek Online wrote about America's Other Pension Problem.

Companies' financial obligations to retiring workers -- in the form of pensions -- have come into the spotlight recently. And despite concern that the pension plans of many companies suffer from underfunding, Americans can take some comfort in the fact that pension funding is regulated by the government and financial accounting oversight bodies. But another, lesser-known obligation may pose an even bigger problem for Corporate America -- funding shortfalls for post-retirement health plans.Local Healthcare Problems

Other post employment benefits (OPEB), as these benefits are known, are receiving greater attention from lawmakers and regulators. On Nov. 10, 2005, the Financial Accounting Standards Board (FASB) unanimously voted to add pension and OPEB treatment to its agenda.

OPEB obligations consist mostly of medical costs paid to insurance companies (or special accounts for the self-insured) and pharmaceutical outfits for the benefit of retired workers. These benefits may be contractual or implied, and usually require retiree contributions in the form of monthly premiums and direct co-payments for services and products rendered.

Unlike with pensions, which are regulated, companies have no legal requirement to create a trust entity to fund the current or future OPEB costs. Additionally, specific tax treatments and credits set up to encourage pension funding do not exist for OPEB funds. For these reasons many companies have not created trust accounts to fund their OPEB obligations, and those that have done so fund them to significantly lower levels than required under current pension funding rules.

Pensions, while underfunded, have 88.3% of their obligations set aside in pension trusts, compared to 21.7% for OPEB obligations. The result: The underfunded OPEB liability of companies in the S&P 500 is significantly larger than the pension underfunding. For the 337 companies in the S&P 500 that offer OPEB, only 282 provided sufficient information for estimates. Those 282 had OPEB assets of $82.2 billion and OPEB obligations of $379 billion, resulting in an underfunding balance of $292.2 billion.

A fundamental difference between pensions and OPEB are that pensions have required funding and the Pension Benefit Guaranty Corp. (PBGC) behind them, while OPEB have no such requirement or quasi-government backing. Another dissimilarity: Over the last two years, additional disclosures for pensions have been added to assist investors in evaluations, while similar disclosure has not been enacted for OPEB.

The underfunding of both pensions and OPEB stems from a combination of low interest rates and specific accounting methodologies designed to smooth out market volatility. Pensions and OPEB, like debts, must be paid if a company is to remain credible. Their obligations are imperative in analyzing and evaluating ongoing concerns.

The FASB initiative's first step, expected to take about one year, will add the net pension and OPEB status to the balance sheet. The second would actually change the methodology of pensions and OPEB, and that will likely take at least three years.

The International Herald Tribune is writing about the healthcare retirement time bomb.

Since 1983, the city of Duluth, Minn., has been promising free lifetime health care to all of its retired workers, their spouses and their children up to age 26. No one really knew how much it would cost. Three years ago, the city decided to find out.Defined Benefit Broken Promises

It took an actuary about three months to identify all the past and current city workers who qualified for the benefits. She tallied their data by age, sex, previous insurance claims and other factors. Then she estimated how much it would cost to provide free lifetime care to such a group.

The total came to about $178 million, or more than double the city's operating budget. And the bill was growing.

Mayor Herb Bergson was more direct. "We can't pay for it," he said in a recent interview. "The city isn't going to function because it's just going to be in the health care business."

Duluth's doleful discovery is about to be repeated across the country. Thousands of government bodies, including states, cities, towns, school districts and water authorities, are in for the same kind of shock in the next year or so. For years, governments have been promising generous medical benefits to millions of schoolteachers, firefighters and other employees when they retire, yet experts say that virtually none of these governments have kept track of the mounting price tag. The usual practice is to budget for health care a year at a time, and to leave the rest for the future.

Off the government balance sheets - out of sight and out of mind - those obligations have been ballooning as health care costs have spiraled and as the baby-boom generation has approached retirement. And now the accounting rulemaker for the public sector, the Governmental Accounting Standards Board, says it is time for every government to do what Duluth has done: to come to grips with the total value of its promises, and to report it to their taxpayers and bondholders.

"It's not going to be pretty, and it's not the fault of the workers," said Mayor Bergson, himself a former police officer from Duluth's sister city of Superior, Wis. "The people here who've retired did earn their benefits."

The new accounting rule is to be phased in over three years, with all 50 states and hundreds of large cities and counties required to comply first. Those governments are beginning to do the necessary research to determine the current costs and the future obligations of their longstanding promises to help pay for retirees' health care. Local health plans vary widely and have to be analyzed one by one. No one is sure what the total will be, only that it will be big.

Stephen T. McElhaney, an actuary and principal at Mercer Human Resources, a benefits consulting firm that advises states and local governments, estimated that the national total could be $1 trillion. "This is a huge liability," said Jan Lazar, an independent benefits consultant in Lansing, Mich. "If anybody understands it, they'll freak out."

The LA Times is reporting on Broken Promises of defined benefit plans.

On October 8th October 8 Delphi Chief Executive Robert S. "Steve" Miller, citing global competition and crippling "legacy costs," ushered the $28.6 billion-a-year company into one of the largest industrial bankruptcies in U.S. history. In short order, Miller called for slashing workers' compensation by almost two-thirds, threatened to void the company's union contracts, and hinted broadly that he would follow the playbook he had used elsewhere of pushing responsibility for paying the firm's pensions to the federal government and dumping its retiree health benefits altogether.Defined Benefit Plan Participants

Since 1980, the fraction of the full-time private sector workforce covered by pensions has fallen from 35% to under 20%, according to the Employee Benefit Research Institute, which is sponsored by big business.

One in every six to 10 companies that still offer pensions have frozen their plans by limiting or eliminating employees' right to accrue additional benefits or no longer covering new hires, according to studies by the Pension Benefit Guaranty Corp.

In a nutshell, America is quickly converting from a defined benefit society to a defined contribution one. Explanations for why such a deep-running change is occurring vary widely. In Delphi's case, Miller has said the answer is simple: The firm's competitors don't provide generous pensions or retiree health benefits, so it can't either.

The switch from traditional pensions to 401(k)s is the most clear-cut example of the risk shift underway in America from business and government to working families. But it hardly is the only one.

Across the country, safety nets that working people once depended on to shield them from economic dislocation — for example, unemployment compensation, disability insurance, job training and healthcare coverage — have been scaled back or eliminated. At Delphi, the battle lines have formed not just over retirement, but also wages, benefits, job security, indeed the company's very survival.

Until the last few years, they could have rested easy that the Pension Benefit Guaranty Corp. would ensure that they got paid. But that was before many of the nation's steel companies and some of its biggest airlines declared bankruptcy and dumped their pension obligations on the government. Among them: Miller-managed Bethlehem Steel, whose retirement promises will cost the pension agency $3.7 billion.

Suddenly, the Pension Benefit Guaranty Corp.'s $9.7-billion surplus in 2000 became a $22.8-billion deficit, and some analysts suggest that this was just the beginning of the trouble.

Seizing on the agency's estimate of a $450-billion mismatch between the assets and liabilities of all of the nation's private pension plans, these analysts say that a financial crisis of the magnitude of the savings-and-loan fiasco of the 1980s is in the offing. Others say that a second, similar-sized crisis is on the way for state and local government pensions, which the Pension Benefit Guaranty Corp. does not insure, but which carry a kind of implicit public guarantee.

Coming atop President Bush's concerns about the solvency of Social Security, the new warnings seem to suggest that America has over-promised; that even if current and near retirees like Montgomery and Seibert get their pensions, younger workers won't get — or even be offered — anything similar; that the era of defined benefit protection is coming to a crashing close.

The big problem is that almost no one in Washington can agree on precisely how to manage it.

Following are a pair of charts on private sector defined benefit plans.

Notice how the number of defined benefit plans as well as the number of active participants have been shrinking. This is a result of small and mid-sized employers dropping their pension plans or shifting to defined contribution retirement plans (such as the 401(k) plan). The total number of participants has increased slightly because pension plans typically pay benefits for the life of the retiree. In the public sector, defined benefit plans have remained the predominant type of retirement plan. That is going to be a huge problem as we shall see later.

Pension Plan Underfunding

Somehow the stock market has, for now anyway, ignored the problems at GM, Delphi, and the earlier dumping of benefits on the Federal Government (taxpayers) by steel companies and airlines, as well as all the other underfundings depicted in the above chart. By the way, those figures are understated since small companies are not included in the totals. The correct number is closer to $450 billion.

Looming much larger but perhaps a bit further out on the horizon are state and local pension plan problems. Many are in serious trouble already with hardly anyone paying attention. Let's take a look.

Statewide Pension Bombs

Focusing on problems addressing states Stateline.Org writes Pensions pose time bombs for budgets.

The aging of baby boomers in the state government work force is prompting fears that pension payouts will bust state budgets and is spurring efforts from Alaska to Massachusetts to reform public employee retirement systems.Did wall Street Wreck United's Pension?

Experts say states, counties and cities are short $292.4 billion in money promised through their public employee retirement systems, makes them ticking time bombs for state and local budgets.

"Folks are really not paying that much attention. ... It's something that warrants far more scrutiny," said Sujit CanagaRetna, a fiscal analyst with the Council of State Governments, a bipartisan umbrella organization for state government officials.

To limit their pension debts, five Republican governors this year championed proposals to mimic the private sector by moving state employees from traditional pension programs -- with guaranteed payouts -- to 401K-style programs, where the state contributes a set amount each month to an employee’s investment fund. When employees retire, the money in the fund is theirs.

But [with the exception of Alaska] their proposals also faltered in the face of fierce opposition from public employee unions, which say the 401K-style plans provide less comprehensive retirement security for state and local government employees.

At least 40 percent of current state employees in 20 states will be eligible for retirement by 2015, according to a 37-state survey released earlier this year by the Government Performance Project. Washington, Maine, Tennessee, Michigan and Pennsylvania will have the most employees reaching retirement age in the next 10 years.

In addition to an aging workforce, CanagaRetna of CSG said other factors are creating unfunded liabilities in state pension programs. For example, states such as Illinois, New Jersey and North Carolina decreased payments into their retirement systems to help balance their books during the fiscal crisis and are now scrambling to catch up, he said.

Currently, the majority of state and local employees are covered by traditional defined-benefit pension plans.

Daniel Clifton, chief economist with Americans for Tax Reform said: "You're not going to have enough new workers to replace the older workers. That's a recipe for fiscal disaster. ... I believe personally it's a pension time bomb waiting to happen."

In what appears to be foolish attempt to gain extra "yield", a common practice these days with everyone assuming the government can and will bail out anyone and everyone that fails, a July New York Times article wrote How Wall Street Wrecked United's Pension.

Hearings have been convened in the wake of United's default, chief executives examined under oath, bills introduced in Congress, numbers crunched. But virtually everyone is looking at the rules covering how much money a company puts into a pension plan every year - not at what happens to the money after that.Sinkholes Drain City & State Budgets

While the money managers and other pension professionals who ran United's pension plan walked away from the wreck unscathed - indeed, they collected about $125 million in fees over the last five years alone, records show - the ones who will have to pick up the bill for the advisers' collective failure will be the airline's 130,000 employees and pensioners, the federal pension guarantor and probably, someday, the taxpayers.

Pension investing is largely unregulated, even though the federal government effectively covers the investment losses when a defined-benefit plan fails. At United, this freewheeling approach gave rise to investments in junk bonds, dot-coms and even what appears to be an energy venture in Albania.

The Securities and Exchange Commission recently said that more than half of the consultants who help pension funds invest their money have outside business relationships that could taint their advice.

Back on June 13, Businessweek wrote about the Sinkhole!Draining state and city budgets.

The public schools in Jenison, Mich., are real gems: Test scores are well above the national average, its autism and special-education program is recognized around the country, and the music program has been honored by the group that hands out the Grammy Awards.Is there a fallback for state and local plans?

But underneath all that success is a looming fiscal crisis. In the past three years, Superintendent Thomas M. TenBrink has surgically cut $4.2 million out of his $39 million budget in a quest to keep Jenison the fiscally responsible district it has long been. He has instituted fees for participating in after-school sports and field trips. He eliminated 30 teaching spots, leaving the district with 287. He hasn't bought a new textbook in three years. He saved $550,000 by turning an elementary school into a self-financing preschool and day-care center. But TenBrink is running out of options.

Jenison is caught in a financial vise. School funds from the state are capped by law at $6,700 per student, a figure that has been frozen for the past three years, but costs are zooming. The fastest-growing outlay of all: contributions to pensions and retiree health care. This year the bill is $1 million. Next year it will jump to $1.5 million. An expense that for years hovered at 12.99% of payroll is now eating up 14.87% of it, and state finance experts predict it will hit 20% within three years. "That is just draining our budgets," TenBrink says.

It's not just school districts that are being squeezed. State and local governments, hard hit by the economic downturn of 2001, find themselves in a financial bind. While sharp anti-tax sentiment constrains revenue and governments face new outlays for everything from homeland security to No Child Left Behind, there's a growing feeling that the retirement promises made to everyone from office workers and state patrols to firefighters and legislators may simply be unbearable. For some of the worst-off states, like Illinois, there is a long history of failure to fund pensions, which have snowballed into multibillion-dollar shortfall.

Recent anecdotal evidence shows that many towns and cities have bumped up taxes over the past few years as state and federal governments have pushed unfunded requirements like No Child Left Behind and other costs down the ladder.

How long that can continue without voter backlash is unclear, however. Meanwhile the cost of retirement has continued its steady climb. According to the U.S. Census Bureau, major public pension plans paid out $78.5 billion in the 12 months ended Sept. 30, 2000. By the comparable period in 2004, that had grown to $117.8 billion, a 50% climb in five years. Beyond hiking taxes and cutting costs, governments have few ways to meet this bill. One option that many fiscal conservatives find troubling is pension obligation bonds. They are, essentially, an arbitrage bet in which governments borrow at relatively low municipal rates, invest the money, and hope they make enough to cover pension payments and earn a bit on the top. But they can lose money if the market goes south, a situation that New Jersey, which issued $2.7 billion in bonds in 1997, now finds itself in. Over the past decade state and local governments have borrowed approximately $30 billion this way.

Don't expect that flood of debt to slow, because there's little relief in sight. Excluding federal workers, more than 14 million public servants and 6 million retirees are owed $2.37 trillion by more than 2,000 different states, cities, and agencies, according to recent studies.

As much as states are throwing into pensions, they may owe even more. Despite a 2004 stock market rise that should narrow some of the gap, pension experts at Barclays Global Investors (BCS ) say that if public plans calculated their obligations using the more conservative math that private funds do, they would not be $278 billion under, but more than $700 billion in the red. "It's just ruining the financial picture for states and municipalities," says Matthew H. Scanlan, managing director of Barclays, one of the largest managers of pension-fund investments. "You're looking at a taxpayer bailout of this pension crisis at some point."

There's more bad news. One major category of cost isn't disclosed at all: how much retiree health care has been promised to public retirees. No one can estimate how much these promises will add up to, but they're sure to be in the tens of billions, and only some states seem to have put aside reserves for them, according to bond analysts. That's chilling, given how quickly medical costs are rising. After a pitched battle, the Governmental Accounting Standards Board (GASB), the independent accounting standards-setter for state and local governments, has finally begun to require states to disclose these liabilities. Numerous unions and state government representatives objected to the change, says GASB member Cynthia B. Green, "not because [unions and states] didn't think these were important, but because they thought once the governments did their studies and found what the price tag was, they would be concerned or, if not concerned, staggered."

In 1998 the city of Houston instituted a deferred-retirement option plan, or DROP, that would allow workers to in effect take their retirement when they became eligible for it but continue to work at their salary. The retirement income was put in a side account where it earned an attractive rate of return, and the employee could later have his pension adjusted upward to a higher level. The DROP, along with other pension improvements, drove the city's pension plan down from 91%-funded in 2000 to just 60% two years later. Houston had gone from contributing 9.5% of payroll toward pensions to more than 32%. Joseph Esuchanko, a Michigan actuary brought in to study the problem, discovered that things would only get worse. According to his calculations, it was possible for employees to become millionaires thanks to the system. Under one scenario, a lifelong city employee retiring with a salary of $92,000 could get $420,000 a year in pension benefits. The citizens of Houston agreed with Esuchanko's conclusion that the system was a "win-win for the employee and a lose-lose for the employer." Last May they voted to end the benefits.

San Diego's mayor, Richard Murphy, announced on Apr. 25 he would resign on July 15 after facing a continuing debate over how to solve the problem and probes by the Securities & Exchange Commission, FBI, and the U.S. Attorney for the Southern District of California's office into securities fraud and public corruption in connection with a crippling $1.4 billion deficit in San Diego's municipal pension fund.

But San Diego is only the beginning. Citizens of Salinas, Calif., where pension costs are up and revenue is down, are facing the possibility that their public libraries will close this year. Orange County, Los Angeles County, and many other California counties have significant pension deficits. The state itself will pay $3.5 billion into pension and health benefits for retirees this year, almost triple what it paid just three years ago. And California's Legislative Analyst's Office (LAO) expects that to climb another $1.1 billion over the next five years.

Take a look at Illinois. The fifth-wealthiest state in total income, Illinois nevertheless has a 30-year history of shirking its pension promises. According to an analysis by the Civic Federation, a Chicago research group sponsored by the business community, since 1970 Illinois has not once paid its annual pension bill in full. Over the next 40 years the state will have to contribute $275.1 billion if it is to reach its goal of 90% funding -- and that's presuming no benefit changes are made. Through bull markets, bear markets, and sideways markets, the state has consistently lagged, and over time those delays have become more and more expensive. The culprit: reverse compounding. A pension plan's obligations are determined in part by the expected investment return on its assets. In the case of Illinois, that is 8%. So for every dollar not added to assets in time, the state is effectively borrowing from the pension plan at 8% interest. That's a high price in today's market, where municipal bonds typically pay closer to 6%. Illinois Governor Rod R. Blagojevich says that if the state follows its current spending plan, it will have paid $220 billion in interest before it fills the hole.

Only now is anyone looking into the problems of State and Local pension plans. Unfortunately it is far too late. Unlike corporate pension plans with the ability to fall back on the PBGC, state and local governments do not have anyone to dump their problems on. That is probably a blessing, at least for some states whose plans are close to being funded. It may be potential nightmare for those in problem states.

Will there be an exodus of people moving from problem states like Illinois with notably bad pension problems if taxes are raised to cover shortfalls?

US Senate passes Pension Bill

On November 16th the Senate passed a bill to shore up private pensions.

The Senate on Wednesday approved far-reaching pension legislation meant to assure that companies with traditional pension plans live up to the promises they make to their workers.Gain Sharing

In the face of new warnings about the future solvency of the nation's private pension system, the bill passed 97-2. Debate now moves to the House, which is expected to take up its version of the legislation next month.

The SeattleTimes is reporting a Gain Sharing perk may cost state billions.

A state pension perk passed by the Legislature nearly eight years ago, with the expectation that it would cost nothing, could sock taxpayers for billions of dollars.How the hell could anyone think that proposal was a "free lunch"? Some of these pension ideas are staggering stupid.

The state actuary estimates that Washington has about a $4.9 billion hole in its pension system. State and local governments are on the hook to make up the shortfall. Nearly half of what's owed can be tied directly to the benefit in question, called gain-sharing.

The cost of the gain-sharing benefit irks legislators because they thought it would be free.

Gain-sharing "seemed like a good idea at the time. For some reason, we did not understand it was going to cost us," said House Appropriations Chairwoman Helen Sommers, D-Seattle.

"Given my background and experience, I must say I don't know how I could have ever believed that it wouldn't cost something. ... It's expensive," said Sommers, one of the sponsors of the law creating gain-sharing and an expert on the state pension system.

State worker and teacher unions are lining up to defend the benefit, which beefs up retirement checks when pension-fund investments do better than expected. The pension system has paid out more than $1 billion since 1998 because of gain-sharing.

Gain-sharing was approved by lawmakers in March 1998 near the peak of the stock-market boom, when double-digit returns from pension-fund investments seemed commonplace.

So the Legislature OK'd a proposal that increased public-pension benefits when investment returns exceeded expectations. Basically, the law says that when the average rate of returns exceeds 10 percent over four years, half of any excess over 10 percent goes to state workers through the pension system.

The way the gain-sharing law was written also created problems. Instead of making any excess cash a one-time distribution, lawmakers essentially allowed it to become part of the base pension benefit for certain public employees.

In other words, for thousands of workers, the money wasn't sent out as a one-time bonus. It became a permanent part of their retirement check.

More State Pension Woes

The Asbury Park Press is reporting States face pension shortfalls.

As the debate grows over the future of Social Security, officials in most states are struggling with a $260 billion gap in another frayed retirement safety net: public pension programs.Stock Market Woes

More than 5.1 million retired teachers, judges, law enforcement and other public employees now rely on public pensions, with another 15 million workers expecting benefits when they retire.

But a period of poor investment returns, rising benefits and states' failures to properly fund their plans have created a gap between assets and benefits in 45 states, according to the National Association of State Retirement Administrators.

In 13 states, the unfunded liabilities exceed their annual general revenue budgets. For half the states, pension fund shortfalls top $3 billion, NASRA said.

The worst-funded plan: the older of West Virginia's two retirement programs for its teachers. For every dollar it has on hand, it owes $3.50 in promised benefits.

West Virginia Gov. Joe Manchin took office in January and immediately called lawmakers into a special session to pass several measures including a proposal to sell $5.5 billion in bonds to fix the state's teachers, state police and judicial pension programs. Voters must approve the bond sale in a special election scheduled for June. If approved, the state's bonded debt ratio would increase from $859 in revenue-supported debt per state resident to $3,900.

In Maine, lawmakers passed a state budget that proposes to sell $450 million in bonds for state pension and social service programs. Kansas, Illinois and New Jersey have also sold bonds.

"This is a very popular strategy," said Sujit M. CanagaRetna, senior fiscal analyst for The Council of State Governments who recently completed a study of state retirement plans. "It's a very favorable interest rate environment, so it's a good time to borrow."

It's also "a little bit like using a credit card to pay your mortgage," NASRA's Brainard said.

According to John Wasik, author of "The Kitchen-Table Investor," and columnist for Bloomberg News the S&P 500 May Drop If Full Pension Debts Disclosed.

Let's assume that the U.S. Congress cuts through a political briar patch and passes a law that forces full disclosure of pension debts.Theory and Reality of 401K Plans

The consequences might be stunning.

Companies with poorly funded pension plans might have to contribute billions of dollars more to their retirement plans and touch off worker demands that employers pony up even more money for their retirement security.

Just as surely, investors would punish companies with the highest retirement debt, according to a study by David Zion and Bill Carcache, analysts for New York-based investment bank Credit Suisse First Boston. They examined the effect of fully disclosing and accounting for the pension liabilities of the 374 companies in the Standard & Poor's 500 Index with defined- benefit plans.

``We estimate that would cause the total shareholder's equity for the companies in the S&P 500 to drop by $255 billion, or 7 percent,'' they wrote in their Nov. 10 report. The 18 most underfunded companies would fare worse, suffering a 25 percent reduction in shareholder's equity.

Equity Wiped Out

Zion and Carcache figure that shareholder equity -- a company's total assets minus total liabilities (which should include what it owes its pension program) -- would be wiped out at the seven S&P 500 companies with the biggest funding gaps in their pension plans.

This accounting muddle is huge. The Credit Suisse analysts said that pension assets and liabilities are treated as ``off- balance sheet'' items, which distort how much a company really earns and holds in corporate assets. They estimate that only 21 percent of the $1.3 trillion in S&P 500 pension fund assets are currently reported on balance sheets.

There is no way that employees or investors now can discern total pension debts since companies don't have to report their so-called 4010 liabilities to the public. That's the amount owed if a company terminates its defined-benefit plan and has to buy annuities for workers.

Full disclosure usually illuminates boardroom secrets and in this case might lead to changes.

Companies that conclude that their defined-benefit plans are too expensive might trigger freezes or shutdowns of old- style pensions. Pension-fund managers may even sell stocks to reduce the overall risk profile of their portfolios and buy bonds or other securities.

Once the market gyrations subside, I think the outcome for future retirees will be even more challenging.

Ultimately, knowing how pensions are funded will force investors large and small to educate themselves. They will also need to focus more on lowering risk and expenses to better achieve their retirement goals. No matter what the political or economic climate, that's a sound practice.

Back in March of 2005 the Washington Post wrote about the Theory and Reality of 401K plans.

In theory, 401(k) plans and other tax-preferred savings programs can provide a good retirement fund -- if the worker joins up, contributes a substantial chunk of his or her pay, makes the right investment choices and doesn't drop out or tap the account for non-retirement expenses.How far is $10,000 going to go in retirement? How about nowhere?

That's the theory. The reality so far isn't pretty. Today, the median account balance - median means the midpoint, that half are larger and half are smaller -- of 401(k) and individual retirement accounts combined, for households headed by someone 55 to 59 years old, "on the verge of retirement," is about $10,000, the Brookings Institution's Peter Orszag noted last week.

Bob Chapman writing for Goldseek.Com had this to say about the pension crisis:

Almost all public pension plans are underfunded, some by 80%. They are not covered by the PBGC. It will be interesting to see how these pensions are handled. Some employees after 30-years will get 90% of their final salary. For a commander in a police department that is $100,000 a year. In faltering San Diego six board members are accused of making a deal to let City Hall underfund the pension system in return to agreeing to higher benefits for themselves. Explicitly or otherwise, this is what unions and legislators have been doing all over the country. That is conflict of interest and it’s a felony.Solutions?

Forty-four million are covered by private-sector plans and half are already retired and are collecting benefits. Only 50% of active employees support the entire system, which means in 30 years the system will die a natural death because it was actuarially unsound in the first place.

To fix the problems multiple things can happen and none of them will be particularly good for boomers:

- Retirement age has to go up

- Tax rates have to go up

- Benefits have to decline

- Services have to suffer

- Defaults

The Cockroach Theory

Is that the full extent to this mess? Of course not. There is the seen and there is the unseen. The cockroach theory says that for every problem you see there are at least two more hiding somewhere. In fact there are a couple more roaches that we have not even talked about yet.

What happens if just as boomers are about to retire and need cash the stock market goes into a protracted slide? Certainly the market is vulnerable and overly dependent on a housing boom that seems to have stalled. What happens to the stock market as boomers retire and no longer contribute to it but start pulling cash out? How far away is that? Are other savings sufficient? I think not. Too many people expect the value of their house to rise forever and bail them out. Just who will the boomers be selling to anyway? If taxes rise to pay retirees will active workers be able to bear the load? What about pension plan assumptions at GM and IBM and other places that are close to 10% while bonds are yielding 4%? Has a demand for yield forced money into junk bonds and other risky investments to meet those expected returns? I think so, so what happens when that unwinds?

Questions, Questions, Questions.

Unfortunately there seems to be a lot of questions but few good answers.

Ready or not the Baby Boomer Bombs are about ready to go off.

Are you prepared?

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/