Where the hell are the jobs?

Mish Moved to MishTalk.Com Click to Visit.

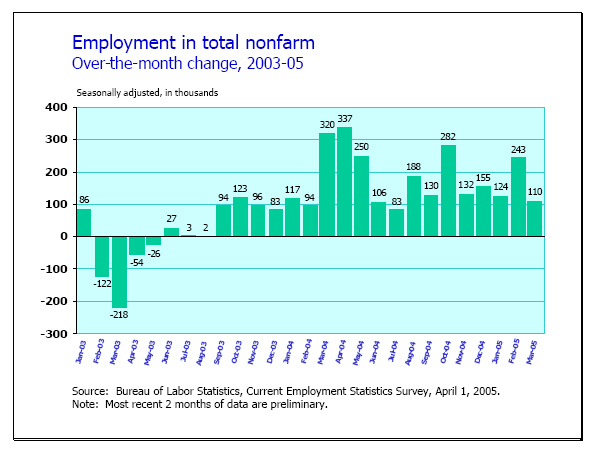

Following is a chart of month to month non-farm payroll job gains or losses since January 2003.

Since it takes 150,000 jobs a month just to keep up with the birth rate and immigration, anything less than that and we are actually losing jobs no matter what the hype from CNBC says. A quick glance at the above chart clearly shows that jobs have not kept pace with the birth rate in 16 out of the last 23 months.

Looking at the most current data, jobs have not kept pace with the birth rate in 6 out of the last 10 months. In other words jobs have not kept up with the birth rate ever since the FED started tightening. In terms of job creation, this has been one pathetic recovery to say the least.

Enquiring Mish readers might be wondering about manufacturing jobs.

Here is the sad story:

The above chart clearly shows that the US has lost manufacturing jobs in 8 out of the last 10 months, and 18 out of the last 23 months. That statistic does not even attempt to factor in the affects of population growth.

Here are the month to month manufacturing ISM numbers since 1948. Since any number over 50 correlates to manufacturing "expansion" and since we have been "expanding" for 33 out of the last 38 months, what happened to the jobs? We will get to that question in just a bit but let’s consider some additional data first.

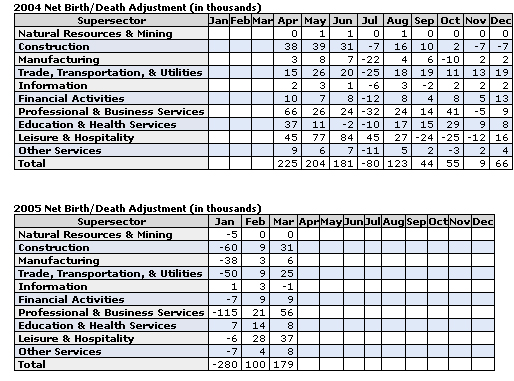

Following is a chart of the CES "birth/death model" . For those not familiar with the birth/death model, the US Bureau of Labor Statistics (BLS) makes assumptions during recoveries about how many new businesses are being created and how many people are hypothetically employed by those new businesses. Every month they add or subtract jobs according to what their model says. No one really knows whether or not these jobs really exist, it is all a figment of someone's imagination and the number of jobs the model thinks should be created during a typical recovery. Well one of their problems is this is not a typical recovery but so far the fine folks at the BLS have not yet waken up to that fact.

Birth/Death adjustments 2004-2005

Take notice of January and July. Those are the "revision months" where the BLS makes adjustments if they think their model was off in the previous months. Year in and year out the BLS adds fictional jobs 10 months a year then subtracts some of them in January and July. In January 2005 the BLS subtracted 280,000 jobs they assumed in the prior 5 months and in July of 2004 they subtracted 80,000 jobs they previously presumed existed. For several years now the pattern has been a month to month overstatement of about 30%. Of course the administration, economic cheerleaders, and analysts get the benefit of over-hyping jobs 5 out of 6 months before making corrections during the 6th.

Bear in mind that no one knows if any of those jobs were really created or not. They are merely assumed to exist. The BLS has a "recovery model" that says such and such a number of jobs SHOULD have been created so they just add them to the monthly job totals as if they were created. To be fair, in a typical expansion there are new companies being created and those companies do not immediately show up in other BLS data. One has to wonder, however, given the obvious job creation difficulties of this "recovery", just how overstated their birth/death model is, even after they make the twice annual corrections.

Notice that the BLS assumed that 179,000 new jobs were created in March 2005. Next take a look at the headline job number for March:U.S. March nonfarm payrolls up 110,000 Nowhere does anyone tell you that of those 110,000 jobs, 179,000 of them were assumed! Without that assumption, we would have lost 69,000 jobs in March!

Looking at the Establishment Data Archives for 2001 and 2004 we can see that in January 2001 when Bush first took off there were 132,129K total non-farm jobs and 111,661K of them were private sector.

In December 2004 there were 132,449K total non-farm jobs of which 110,749K were private sector jobs. Hmmm. It seems to me that we actually flat out lost 912K private sector jobs between January 2001 and December 2004. President Bush avoided winning the "Hoover Award", the first president since Hoover to lose jobs on his term only because of military expansion and government jobs.

Given the above charts and stats (all using the Governments own data I might add) enquiring Mish bloggers just might be wondering "How the hell can the unemployment rate be dropping?". That certainly is a fair question and the answer is hidden in the "participation rate". Even though we need to create 150,000 jobs a month just to keep up with the birth rate, unemployment can drop when benefits expire and people fall off the rolls. This affects something called the "participation rate" and it has been dropping like a rock even though in a normal recovery it should be increasing. The BLS definition of the "participation rate" is the labor force as a percent of the population. The participation rate was 67.5% in January of 2000 and was 65.8% in March of 2005. This sleight of hand magic would make all the crowing about the unemployment rate dropping to 5.2% laughable except for the fact that people seem to believe the headline unemployment rate as reported every month. If you know people that are wondering why they can't find a job when "everyone else" seems to be finding a job (as reported anyway) please send them to this post for a proper explanation of how they are being lied to.

If one scrolls down to table A-12 Alternative measures of labor underutilization, once can see that a more accurate measure of unemployment is somewhere between 6.2% and 9.1%. Now call me skeptical, but since that is the number the BLS is willing to admit, I am willing to speculate the actual number may be a lot higher. At any rate, the 5.2% reported in March 2005 is a total fabrication.

No doubt Greenspan is in a conundrum over the lack of job creation during this "recovery", but I have a hunch that most Mish bloggers know what happened. Jobs indeed were created but in India and China and not in the US. With manufacturing wages of $1 per hour in China and $32 per hour here, it is surprising we have any manufacturing jobs left at all. The US textile industry is bitching to high heavens about this and it certainly is easy enough to hop on the "China Bashing Bandwagon", but unfortunately that is not where the solution lies.

To save 500 underwear manufacturing jobs in the US we would have to place enormous tariffs on goods from China. Does everyone want to pay 5 times as much for underwear to save a lousy 500 US textile jobs? Do people want to pay 3 times as much for a "made in the USA" television set or are they addicted to cheap goods from China? Everyone seems to like a bargain or the masses would not be shopping at Walmart and Target and Best Buy etc.

Point blank the problem is simple: wages are not keeping up with US consumer spending habits and people are making ends meet only by treating their houses as an ATM to support consumption. The model is not sustainable and re problem rests squarely on Greenspan and the FED. Rather than let the normal business cycle play out, Greenspan destroyed the US$ by slashing interest rates to 1%. This fueled the exportation of jobs to China and India and led to an unsupportable boom in housing in the US.

Ceri Shepherd discussed how We Are Outsourcing Ourselves just today in a fine article that I suggest everyone should read.

The point to ponder is this: Since we created practically zero net jobs to speak of during this "recovery" in spite of the fact that we had a booming housing market for three years, just what happens WHEN (not if) housing goes bust?

Since I have been harping the same story as Ceri for years perhaps it will do some good to hear it from someone other than myself for a change. From Ceri:

"It is my belief that many westerners are going to be given a hard lesson in property deflation which is the inevitable end game of property inflation, caused by using large amounts of credit or leverage chasing perceived price gains. When the market inevitably turns down it quickly becomes a very illiquid market as the credit and buyers dry up, inflation then becomes deflation.

It will also be interesting to see how many of the “investment properties” cascade into the market, at exactly the wrong time when the downturn starts. I suspect that not only will the “homeowners” be upside down on there auto loans but also on there mortgages as well. It is also very probable that many of the banks, GSE,s and holders of securitized mortgage debt will also be upside down."

Unfortunately for the US there is no way out of this mess. Talk of "soft landing" at this point is sheer nonsense. The excesses of the past 20 years have fueled bubble after bubble after bubble. Everyone thinks "A property bust can't happen here" because we are "different than Japan" and that housing will "always come back" are in for the same rude awakening that investors in JDSU saw when they thought the growth in fiber would last forever.

The only thing Greenspan has been successful at during his lengthy career is blowing bigger bubble after bigger bubble. The end is now at hand because the magic bubble pipe has run dry. There will be no bigger bubble bailouts when this one pops.

I will leave you with three facts:

1) Housing can not keep going up faster than wages.

2) Every credit boom in history has ended in a deflationary bust.

3) It's NOT different this time.

Mish