Someone recently sent me a set of articles that appeared on the Motley FOOL and asked for comments. All three were written by the same person: Mike Norman.

The first article is called Tune Out the Debt Doomsday Crowd.

Following are a few snips:

Have you ever seen one of those debt clocks? They show our national debt, with the numbers ticking away at the end so fast you can't even read them.

The debt is a source of popular conversation again, now that it has hit a new high of $8.4 trillion. And of course, it's never been out of favor with the Debt Doomsday crowd. I'm sure you know those folks. They're the ones who have been predicting a debt-driven collapse of the U.S. economy for decades -- yet it's never happened.

Much ado about nothing

I'm going to let you in on a little secret: The U.S. debt is tiny. That's right, tiny. Take a look at this: The $8.4 trillion figure is only about two-thirds of our nation's economic output, which is currently at $13 trillion and growing.

For those of you wondering who took the dubious top honors in the world of national debt, it was Uruguay, with a debt-to-GDP ratio of 793%!

For America, however, the debt news is really better than it appears. Of the $8.4 trillion that the government owes, $3.5 trillion is intragovernmental debt -- or what the government owes to itself. Essentially, this is all bookkeeping, and operationally never a cause for worry.

When you look at that as a percentage of GDP, however, it comes in at a very comfortable and manageable 38%, which is well below the post-World War II average of 43%.

I hardly know where to start. Comparing the US to Uruguay and proclaiming "see look how much worse someone else is" is hardly a decent measure of fiscal sanity.

Next, Norman has his figures wrong.

In

Is the US dollar toast? I have a graph of the National Debt from Whitehouse.Gov showing the projection by the OMB to be close to 70% and nowhere near "a comfortable manageable 38%" that Norman proclaims.

The chart above shows the debt to GDP ratio was higher under Truman. But this was in the wake of WWII and with the baby boomer boom just starting. The debt to GDP ratio is now close to a peace time record high (if one calls this peace) and far exceeds the Vietnam Era debt to GDP ratios under LBJ and Nixon. Will there be another baby boomer boom to bale us out? I think not.

Please consider the following paragraphs from the May issue of the Richebächer Letter as mentioned in

Ostrich of Omaha.

Over the five years from 2000–2005, total debt, nonfinancial and financial, has increased $12.7 trillion in the United States. This compares with a simultaneous rise in national income by $2.1 trillion. For each dollar added to income, there were $6 added to indebtedness.

In real terms, national income increased little more than $1 trillion. Last year, U.S. private households added $374.4 billion to their disposable income and $1,204.7 billion to their outstanding debts. Inflation-adjusted disposable income grew $115.7 billion. It is a growth pattern with exploding debts and imploding income growth.I must point out that Richebächer was talking total debt, not just government debt. Personal debt is indeed a bigger problem right now but that does not mean government debt is a non-issue. It boils down to a question of timing. What matters more (right now) is personal debt but that does not necessarily make government debt "comfortable". When the baby boomer time bomb triggers, there will likely be nothing comfortable at all about government debt, especially if current deficit spending continues and there are fewer workers supporting each retiree.

As Richebächer points out: Every year it takes more debt (public and private) to produce equivalent GDP growth. Every year it takes more debt to produce fewer jobs than any recovery before it. Every year the percentage of GDP it takes to finance that debt increases. To those ideas I would like to add, that every year the government attempts to hide more and more expenses (such as the war in Iraq) off the balance sheets.

Furthermore, estimates of US GDP are total fabrications of reality. For those that want to tout GDP and US growth compared to the rest of the world, I suggest reading

Grossly Distorted Procedures.

Yes, Japan does have a higher (way higher) percent of debt to GDP than the US. But guess what? I have been told by many people that it is OK because the "Japanese owe it to themselves". The idea that debt is OK because we "owe it to ourselves" is nonsensical. I will have a lot more to say about "owing money to oneself" in a rebuttal of "America IS Fiscally Responsible", Norman's next article.

Monetary nonsense is running out of hand yet people believe what they want to hear. What people want to hear are the "free lunch" ideas that Norman is spouting.

Yes, "It hasn't mattered yet".

All I have to say is "How comforting".

Until the great depression happened, that had not happened on a worldwide scale ever before either. Until the Nasdaq collapsed 75% that had not happened either. Until gold rose from $35 to $800 that had not happened either.

Point blank, arguments that suggest something can not happen because it has not happened yet are silly. Yet consider these facts:

- We have had a great depression

- We have had an Nasdaq crash

- We have had interest rates rise to 18%

- We have had interest rates fall to 1%

- Japan did have a stock market that fell for 18 years

- Japan did have real estate prices that fell for 18 consecutive years

Until those happened they had not happened before.

Worse yet, there is now a precedent.

If they happened once, they can happen again.

If it happened in Japan it can happen here.

America IS Fiscally Responsible

Norman Proclaims

America IS Fiscally Responsible.

Why deficits are good

While it's true that the nominal figures have grown, it's a mistake to examine the deficit and debt numbers without some frame of reference. That frame of reference is how big the economy has grown. To ignore the growth in inflows (or the asset side of the balance sheet) gives a totally lopsided view. It's as if you walked into a bank to get a loan and only showed the loan officer a list of your debts. In the real world, the banker would have the sense to also demand to see how much money you made and a list of the assets you owned. When it comes to the government, however, the Debt Doomsday crowd doesn't want you to know about the income and asset side of the balance sheet. All they want you to see is that big, scary debt figure.

Beware of fearmongering

The fact of the matter is that unless we decide to end the growth policies that have been driving this nation's economy for the past two centuries, we shall be leaving the same or even more riches to our children and our grandchildren than we'll inherit from our parents. It's always been that way -- and it's the reason why all the worries about the Social Security and Medicare "time bomb" are misplaced. Do you realize that those dire forecasts have been around almost since Social Security's inception back in the 1930s? Yet they have never come to pass.

Once again we see the same reasoning that "It hasn't happened yet" so ignore it. Of course it hasn't mattered "yet". The condition that triggers the Social Security problem is a massive Baby Boomer Retirement and that has not yet happened. But it is about to.

Back in March I reviewed US Government’s consolidated financial statements for the fiscal year ending September 30, 2005, a 158 page PDF, and reported on it in

The Sorry State of US Govt Accounting Practices.

The federal government’s fiscal exposures now total more than $46 trillion, up from about $20 trillion in 2000. This translates into a burden of about $156,000 per American or approximately $375,000 per full-time worker, up from $72,000 and $165,000 respectively, in 2000. Please note that was not my comment, but a comment by David M. Walker, Comptroller General of the United States. Here are my comments.

We Owe It To OurselvesWhat the US is doing can be equated to taking money out of a piggy bank (a piggy bank that should be accumulating cash to pay for future known liabilities) , spending that money now, but putting an IOU slip back in the bank and suggesting this makes perfect accounting sense because we "owe the money to ourselves".

The idea is preposterous. Espousing ideas that suggest things are OK because we "owe ourselves money" is no more "contrarian thinking" than it would be for a math teacher to write+1=3 on the blackboard while calling it "contrarian math". Any math teacher suggesting 1+1=3 would be promptly fired. Any would be economist suggesting that everything is OK because "we owe ourselves money" should be fired as well. It is impossible to owe oneself money.

Following is another statement signed off by Walker, the US Comptroller General:

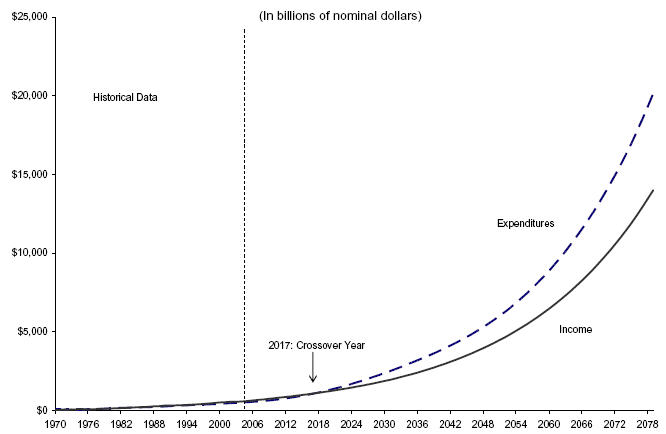

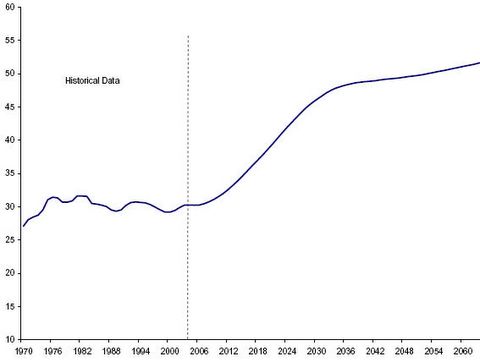

More troubling still, the federal government’s financial condition and long-term fiscal outlook is continuing to deteriorate. While the fiscal year 2005 budget deficit was lower than 2004, it was still very high, especially given the impending retirement of the “baby boom” generation and rising health care costs. Importantly, the federal government’s accrual based net operating cost increased to $760 billion in fiscal year 2005 from $616 billion in fiscal year 2004. Social SecurityIn 2004, there were about 30 beneficiaries for every 100 workers. By 2030, there will be about 46 beneficiaries for every 100 workers. A similar demographic pattern confronts the Medicare Program. For example, for the HI Program, there were about 26 beneficiaries for every 100 workers in 2004; by 2030 there are expected to be about 42 beneficiaries for every 100 workers. This ratio for both programs will continue to increase to about 50 beneficiaries for every 100 workers by the end of the projection period, after the baby-boom generation has moved through the Social Security system due to declining birth rates and increasing longevity.

A chart for Social Security showing the number of beneficiaries per 100 workers can be found on page 54 of the 158 page PDF:

Social Security Expenditures minus Income

Social Security Expenditures minus Income

One quick look at those charts should be proof enough of the silliness of the "no problem yet" crowd. As bad as Social Security looks, Medicaid/Medicare looks worse. Those interested in real facts, should click on the previous link and see what the Comptroller General of the United States is worried about. Norman may not be worried, but the Comptroller General seems worried and you should be worried too.

As for "ignoring the asset side of the equation", Norman's arguments are easily dismissed. Heading into the Nascrash of 2000 assets were high. What happened to those assets? They plunged right? Did debt go away? No it did not. We are in the same situation now, only worse. Greenspan and Bernanke replaced one bubble (in the stock market) with multiple bubbles (housing, stock market, debt).

When assets rise 100% and debt rises 100% what has really happened is that leverage and risk have increased exponentially. What happens if home prices fall a mere 20%? What happens if the stock market falls 40% from here? What happens if real estate prices fall for 8 consecutive years? (Remember they fell 18 consecutive years in Japan). Of course people like Norman say "It can't happen" or "It can't happen here" even though such things have already happened before.

In effect, Norman is suggesting "It's different this time". That argument has a historic 100% failure rate. I do not buy it. Nor should you buy it either, given that home prices are in many places 4 to 5 standard deviations above normal as compared to both rent and wage increases.

History has proven time and time again that housing prices will revert to the mean. When that happens it will make a mockery of those touting the "asset side of the equation".

We are now facing the housing equivalent of the "mother of all margin calls" for leveraged debt backed up only by housing prices expected to rise forever. The ramifications of that "margin call" will be enormous.

Consumers have never been in worse shape from a debt standpoint or so dependent on rising house prices. When home prices plunge, asset values will be wiped out but the debt will remain. Compounding the problem is the "bankruptcy Reform Act". That act is an attempt to make people debt slaves forever.

Is America Bankrupt?In July of 2006 the St. Louis Fed dared to raise the question

Is the United States Bankrupt? Here is the conclusion:

There are 77 million baby boomers now ranging from age 41 to age 59. All are hoping to collect tens of thousands of dollars in pension and healthcare benefits from the next generation. These claimants aren’t going away. In three years, the oldest boomers will be eligible for early Social Security benefits. In six years, the boomer vanguard will start collecting Medicare. Our nation has done nothing to prepare for this onslaught of obligation. Instead, it has continued to focus on a completely meaningless fiscal metric — "the" federal deficit — censored and studiously ignored

long-term fiscal analyses that are scientifically coherent, and dramatically expanded the benefit levels being explicitly or implicitly promised to the baby boomers.

Countries can and do go bankrupt. The United States, with its $65.9 trillion fiscal gap, seems clearly headed down that path. The country needs to stop shooting itself in the foot. It needs to adopt generational accounting as its standard method of budgeting and fiscal analysis, and it needs to adopt fundamental tax, Social Security, and healthcare reforms that will redeem our children’s future.

The Trade DeficitLet's now consider Norman's third article in the series. This one is entitled

How Big Is Your Trade Deficit?Twin deficits will kill us?

This is my last in a series of articles, for the time being, on debt and deficits. I've already written about the budget deficit and the national debt, and I hope you now have some better perspective on those issues, so that the next time you hear the typical one-sided commentary, you'll be better equipped to analyze the arguments. Today, I'd like to discuss the trade deficit.

Reality check

Although we had a $710 billion outflow because of our big import tab, foreigners pumped a whopping $1.2 trillion in investment into our economy. They were snapping up Treasury bonds, stocks, and non-governmental bonds, and putting them into other forms of direct investment. The $1.2 trillion figure more than covered the $710 billion trade deficit, but as usual, the media and the so-called "experts" focused only on the red ink and not the good stuff happening on the financial side.

Yes, the media and the "experts" did talk about those capital inflows, but they totally mischaracterized them by saying that it was simply a case of foreigners "financing" us, and that it was only thanks to their largesse and generosity that we can continue with our profligate ways.

Baloney!

Nobody forces foreigners to invest in America. It's a free, global economy, and they can invest their money anywhere they want. But they put it here because the U.S. economy is the world's engine of growth. Foreign nations -- particularly Asian nations -- have been growing their economies and creating jobs for their citizens by selling products to America. In some cases, this has been going on for decades. In fact, some nations have become so dependent on this form of export-driven growth that they have engaged in all forms of protectionism, including impediments to trade and the costly manipulation of their currencies to maintain a competitive advantage.

At this point, you may be thinking, "Well, haven't they beaten us at the game, then? After all, Mike, you just said they've secured a competitive advantage."

The answer is no -- they haven't beaten us. All they've done is gain an advantage in exports, but it comes at a tremendous cost to their citizens' standard of living. Because to gain that advantage, they've had to divert vast amounts of the money they've earned toward protecting their markets, subsidizing certain industries at the exclusion of others, and keeping their currencies weak relative to the dollar, thereby reducing or suppressing their workers' purchasing power. That's not only inefficient; it's also unsustainable in the long term because it leads to an ever-widening gap between their living standards and those countries where economies are open, as in the case of America. Another way to state it is that imports are a benefit, while exports are a cost.

For the third time we see arguments that equate to "It's different this time". This one suggests that outsourcing of jobs to India and China is a result of strength in the US economy. I strongly disagree. Outsourcing of manufacturing jobs that are replaced with jobs at Walmart can hardly be a good thing.

In the classic sense, savings are what is left over from production after consumption. Given that the US is now a nation of consumers as opposed to producers, any idea that equates consumption as opposed to production as a position of strength is fatally flawed. The US savings rate hit a negative rate of -1.7% the lowest since the great depression. Is that strength? Is it remotely sustainable? The fact that US consumers must grow increasingly indebted to maintain their lifestyle is ample evidence of the unsustainable nature of the current trend. It seems that Norman, like others before him, is making the classic mistake of confusing "savings" with unwarranted asset price inflation caused by "bubble economics" and reckless expansion of credit.

Miscellaneous points of contention - Norman accuses foreign countries of protectionism and subsidizing producers. The fact is few countries are worse than the US when it comes to subsidizing markets. Price crop supports should be proof enough. Look also at Boeing and Halliburton. They are being subsidized by a war in Iraq that did not need to be fought. The same can be said for all weapons manufacturing. Brazil offered to sell us ethanol 35 cents cheaper than we can make it ourselves. We refused the offer and instead our government pays a subsidy to produce ethanol from corn, the least efficient method of ethanol production. When it comes to subsidies the best the US can be accused of is "the pot calling the kettle black". A case can be made that we are worse than anyone but Europe. The beacon of free trade is New Zealand. We should aspire to that standard.

- The idea that the standard of living in China and India is falling is absurd. The fact is the middle class in China and India is rising exponentially while ours is arguably shrinking.

- Real (inflation adjusted) wages have been falling in the US while rising elsewhere. That is unprecedented in an "economic recovery" and is proof that purchasing power in the US is falling.

- An increase in jobs and wages elsewhere (in conjunction with a falling US dollar) suggests that purchasing power outside the US is rising not falling.

- The idea that "imports are a benefit, while exports are a cost" is unsound thinking. It overlooks the destruction of real capital at a rate that is nowhere near sustainable.

Foreign investment in the USForeign governments are buying Treasuries because they do not know what else to do with balance of trade dollars, no more, no less. Anecdotal evidence of that statement is easy enough to establish: China tried to buy Unocal, but Congress interfered. Foreign governments have been trying to buy US port operations but Congress blocked that too. So exactly what are they supposed to do with those dollars? Buy oil you suggest? OK if China uses those dollars to buy oil, what does Saudi Arabia do with those US dollars?

The bigger the US deficits are, the more US assets foreigners are going to buy (or try to buy). So foreigners eventually do have to buy US assets (or the balance of trade has to reverse) which is in stark contrast to the statement

"Nobody forces foreigners to invest in America".

Is it a good thing for China to own Unocal, or Dubai to own US ports, or other countries to be buying US toll roads? This question was explored in

USA For Sale Part 2 . Eventually the US is going to be selling off more and more assets to foreigners whether we like it or not.

We have no choice. That fact that we are selling off the US piece by piece because we have to (not because we want to) is further proof that our current consumption binge is not sustainable.

For now foreigners have been willing to finance our deficits for a mere 5% interest rate. While I suspect this can continue for a while it is a big mistake to assume this arrangement will last forever. The only solution will be to sell off more US assets, stop spending, or hope to god the rest of the world gets as crazy as we are about buying stuff on debt. The latter will only help us if we have a manufacturing base in the US.

The imbalances that Norman says do not matter are about to. A consumer led recession is coming our way regardless of what we do now but the real price to be paid will come later, when China and India no longer need US consumers to grow.

About Mike Norman:Fool contributor Mike Norman is founder and publisher of the Economic Contrarian Update and is a Fox News Business contributor. He also is a radio show host at BizRadio Network.Final ThoughtsOn one hand I am disappointed that the FOOL published those articles by Norman. The reason I am disappointed is because those articles are filled with factual errors while espousing the "free lunch" economic thinking that has this country in the mess that it is in. Some of those ideas are not "contrarian", they are pure nonsense. Thus the printing of such articles on the grounds of "equal time" is no more valid than it would be to give "equal time" to the flat earth society. At the very least the FOOL might have caught some of the factual errors and the "we owe it to ourselves" silliness. I fear for people that take Norman's message to heart. On the other hand, perhaps I should thank the FOOL and Norman as well because the viewpoint "no problem yet" is so pervasive in current thinking that rebuttals like this need to be heard. On that basis I thank Mike Norman and the FOOL for those posts.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

2006-07-28

2006-07-28 In the months ahead, Econ 101 predicts that the prices of existing dwellings will continue to soften.

In the months ahead, Econ 101 predicts that the prices of existing dwellings will continue to soften.